Fed’s “Pause” Party: What’s Next in September?

TL;DR: The Federal Open Market Committee (FOMC) is keeping rates steady this month, but they’re lining up a potential cut in September if things cool down just enough. Think of it as a “hold” button that’s maybe going to be pressed soon.

What the Meeting’s About

- All eyes on the July policy decision: the Fed funds rate stays stuck between 5.25% and 5.50%.

- That’s the eighth straight session the rates are on freeze, and it’s exactly one year since the rate hit its top stretch.

- Money markets are practically shouting, “No surprises here!” The USD Overnight Index Swap (OIS) curve is shouting that any move will feel like a distant rumor.

Why Hold? And Where Are We Heading?

- The board’s hands are closed for now, but they’re clearly keeping an eye on inflation numbers. If the price‑pushing engine pulls back to the 2% target, they’re ready to start the taper.

- At the same time, the labour market is slipping back into a healthier groove. The U.S. workforce is taking a breath, which is great news for anyone watching the job‑loss chats.

Hints You can’t Miss

- Both the policy statement and Chair Jerome Powell’s press conference are sprinkled with cues. “Sooner rather than later” isn’t a promise, but it sure feels like a gentle nudge.

- No hard commitments are set in stone. Think of the Fed’s tone like a polite “maybe later” at a dinner table.

Bottom Line

The Fed’s central bankers are basically saying, “We’re keeping things as they are for now, but look at inflation and jobs—we might cut in September.” The market’s mic‑fading says “no action” for the moment, but keep your eyes on September. That’s when the possible price‑cut party could finally move from planning to party mode.

Market Outlook on Rate Cuts

What the trading world’s buzzing about is that the FOMC is getting ready to loosen the reins. Same recent data shows a ripple through the market sentiment – folks are certain that a swing in policy will soon roll in.

Leading up to the September Meeting

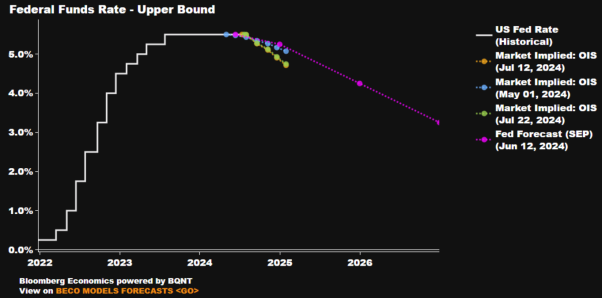

- Odds of a first cut: The curve says there’s about an 87% chance that a rate cut will happen by the September FOMC.

- Total easing by year‑end: Market predictions hint at just over 56 basis points of cuts in total.

That figure? It’s more than twice what the median expectation was in July’s “dot plot.” Talk about a jump! The June forecast might have felt like a cool breeze; now it’s a whole hot‑air balloon ride.

Comparing Past Expectations

Back before that June meeting, the consensus was pretty lukewarm. Markets thought there was a 2‑in‑3 chance of two cuts happening this year. Now, that probability has sky‑highened.

In short, the market’s mood has gone from “maybe” to “definitely” – it’s all set for a more dovish trajectory. If you’re feeling the nine‑panel FOMC uncertainty, you can’t help but grin at the shift toward optimism.

Why the Fed’s Rates Are Jumping Like a Squirrel on a Caffeine Stash

The recent spike in the real fed funds rate isn’t just a random curveball thrown by the market. It’s the result of a triple‑whammy: data proving the disinflation engine is still roaring, cracks starting to show up in the labor market, and a non‑stop tightening of the policy stance.

Key Ingredients of the Repricing Recipe

- Disinflation Confidence Rising – Forecasts keep showing that prices are cooling off faster than a hot cup of coffee on a winter morning.

- Labor Market Cracks – Threats are surfacing in the workforce; think of it as the slow drip of a leaky faucet that could soon turn into a major flood.

- Policy Tightening Continues – The Fed keeps pulling the strings, tightening the regime like a detective tightening clues in a mystery.

Real Fed Funds Rate: The New High‑Light

Using Chair Powell’s favorite method (subtracting the 1‑year inflation breakeven from the nominal fed funds rate), the real rate has surged to about 4.7%. That’s a colossal climb from the modest 1.15% we saw back in Q2, and it tops out the tighter policy stance regime we last saw in late 2018.

It’s a bit ironic, too – just after Powell sparked the famous “autopilot” comment on quantitative tightening, the real rate’s performance shows that the autopilot is far from staying on autopilot.

Bottom Line

Bottom line: The Fed’s got bigger knives in the kitchen, and these numbers hint that their baking will be a lot less sweet in the near future.

Fed’s Rate Outlook: Rates on Hold, Cuts on the Horizon

The Federal Open Market Committee (FOMC) plans to keep interest rates steady for the moment, but their next moves hint that a rate cut is coming, likely as soon as the September meeting.

Why the FOMC Keeps Its Options Open

- They want to stay flexible—no one likes to get stuck in a fixed plan.

- Policy hints will still surface, giving a taste of near‑term normalization without committing fully.

Powell’s Latest Take on the Economy

Chair Jerome Powell says the economy is showing stronger progress toward the inflation target. The “modest” language of the June statement will probably disappear, giving readers a firmer sense that inflation is closing in on that sweet spot.

Labour Market 411

The July notes will also spotlight growing global fragility in the labour market. Risks to the FOMC’s dual mandate—stable prices and full employment—are real, but the balance is starting to tilt in the right direction.

Inflation’s Sweet Spot in Numbers

- Headline CPI: 3% YoY in June—slowest rise in a year.

- Month‑on‑month, CPI fell 0.1%—the first decline since May 2020.

- Core CPI: 3.3% YoY—a drop to its slimmest pace since April 2021.

- Supercore Inflation: 4.7% YoY with a steady monthly dip.

All evidence points to inflation gradually easing toward the coveted 2% mark. That’s the sweet spot the Fed is aiming for, and it’s shaping the guidance for the coming months.

Fed’s Inflation Target: It’s a Long, Bumpy Ride

Even though the numbers keep hovering above the 2% goal, the Committee is pretty much saying, “We’re not chasing that target straight away.” They want just enough confidence that we’ll hit 2% soon enough without getting too fancy about it.

Why the caution? Monetary policy has a famously long and variable lag before it actually nudges the economy. Chair Powell recently warned that if we waited to see a clean 2% inflation beat, we might cut rates too late, leading to an under‑shoot that would annoy both the market and the public.

Labor Market: The First Cracks Show Up

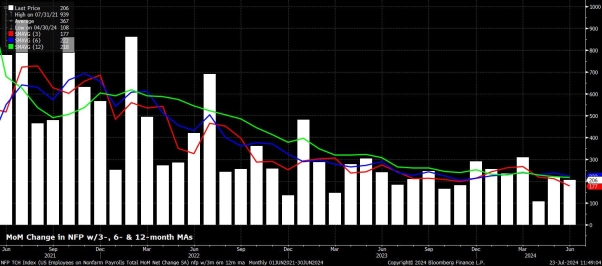

- Headline payrolls rose by 206 k in June – a decent bump that barely beats expectations.

- However, a –111 k revision over the two prior months pulled the 3‑month average job gains down to only 177 k.

- This figure is well below the breakeven pace (about 250 k) needed for employment growth to keep pace with the labour‑force growth. It’s also the lowest 3‑month average of job gains since early 2021.

Those numbers hint that the labour market, which has been surprisingly tight and resilient, is starting to feel the pinch. Will it break or rebound? Time, and a dash of policy humor, will tell.

Jobless Jitters: The Economy’s Slow Drift Back to 2021‑Style Stagnation

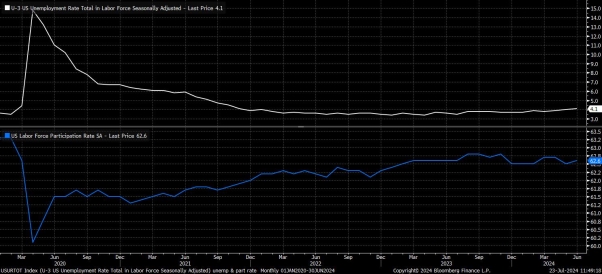

Picture this: the unemployment number climbs to 4.1% – that’s the same figure that didn’t grumble back until November 2021. It’s not a surprise, though, because folks are just throwing more of their ears (the labor force) into the employment pool. So, the headline looks a bit like a “kinda chill” bar, but the glass is actually full.

Why the Numbers are Stirring Up Trouble

- Initial Jobless Claims – up to a 2‑year high. Think of it as a snapshot of people who just stumbled into the unemployment dance.

- Continuing Claims – sitting at the biggest level since November 2021. That’s the long‑term dance floor, still packed from the former economic slowdown.

Powell’s Take: The Market’s Got a Right‑About‑Now Chill Vibe

Chair Powell recently tipped his hat to the market, saying it’s “essentially no tighter” than the situation back in late 2019 – the time when the Federal Open Market Committee (FOMC) were handing out real‑life “insurance” rate cuts. In other words, the market feels as snug as a bag of chips from that vintage.

So, while the unemployment rate is nudging higher, it’s mostly because more people are officially showing up for the job fair. And even though the jobless claim numbers are pointing at more cracks, the overall vibe hasn’t fully snapped back into a crisis‑hot mode yet.

What Powell’s Post‑Meeting Talk Means for You

When Jerome Powell steps off the podium, his words rarely spring from a deep‑secret playbook. He tends to echo what he’s already said in Congress, to his press team, and in speeches over the last few weeks. In short: the recent inflation data is giving the Fed the confidence to keep cooling the economy, and he’s balancing the dual mandate—price stability and maximum employment—like a stand‑up comedian juggling two punchlines.

Key Takeaways from Powell’s Speech

- Inflation is no longer the only danger the Fed faces.

- Risks are now two‑sided; it’s not just about price spikes.

- He’s re‑affirming that rate cuts are coming but will not promise what exactly will happen next.

- During the upcoming election season, Powell will keep his answers straight and non‑political.

Will the Dollar Keep Rolling?

The market’s quick to punish a dovish Fed, so we’re not seeing the USD OIS curve slide dramatically downward. Even though September might bring a rate cut to kick the normalization into motion, the reality on the floor is that markets already expect a slightly faster easing pace than the Fed hints at. Three cuts in as many meetings? That’s basically a “no‑no” answer.

Impact on Stocks

Any hawkish shift in policy will be moderate—nothing dramatic that would choke the equity market. Instead of a big gust that could blow investments away, we’re looking for a gentle breeze that keeps the Fed’s “Fed put” (that built‑in safety net for markets) steady and flexible. This allows investors to stay calm, stay invested, and think of market dips as selling points rather than big scares.

Investor Guidance?

Think of the upcoming July FOMC meeting as the Fed’s way of saying, “Yes, we’re keeping the playbook open.” It’s designed to keep the market quietly confident, letting equities remain poised to climb, while keeping the dollar from taking an unjustified hit.

Stay Updated!

Want real‑time updates on this post category straight to your device? Subscribe now and never miss the next move in the market.