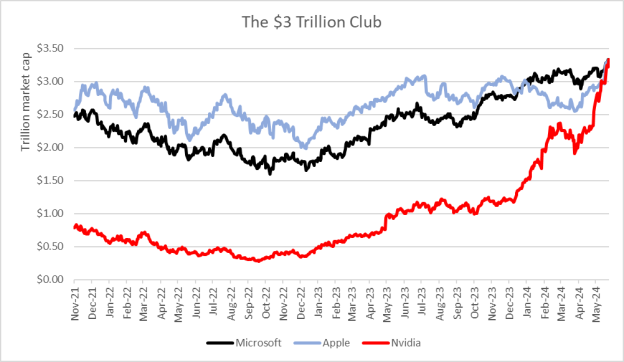

NVIDIA’s Wild Ride: From $2 Trillion to $3 Trillion in Just 96 Days

Every tech‑showbiz fan can’t help but gasp when they see NVIDIA’s ticker tip‑toe past the big‑money line of the world’s stock exchange. Incredibly, the chip‑maker has just become the biggest player on Wall Street – the most tender‑faced, shiny, cash‑loving company in the world.

How Fast is “Fast”?

Picture this: just under three months – 96, to be precise – NVIDIA’s market value jumped from $2 trillion straight up to $3 trillion. That’s like turning a modest chocolate cake into a colossal buffet in record time!

Why the AI‑Bolt?

There’s a hot corner of the speaker boards called the “AI boom.” People keep waving a comparison hand: Apple 2000 vs. now. That’s the same move we used to label the dot‑com frenzy. And, lo and behold, NVIDIA is the new Cisco – the breakout champion of the waves that rocked the internet in the early 2000s.

The Cisco Legacy

Back when Cisco became the first U.S. market titan in March 2000, it turned heads with a staggering valuation of $500 billion. Fast forward to the year 2000, that skyrocketing feature dwindled into the so‑called “bull‑beater” of a bubble. Investors had to wake up to a crisp new reality of corporate values that said, “Yeah, that’s a lot more realistic.”

NVIDIA’s Future?

Thinking about the future, is NVIDIA heading toward a similar steep descent after blowing up? Would the next “AI burst” reflect a sudden stumble, or will it survive with a charismatic, stable chart? The real quest is for shareholders to wait, feel the pulse, and see if the story grows—a carefully plotted, long‑term album that’s popping with company strength rather than a sudden pop‑cardas.

Nvidia’s Sky‑High Surge: Outpacing the Big Four (And Why Your Portfolio Might Be Feeling the Heat)

On June 18, Nvidia exploded past the market caps of Microsoft and Apple, swelling to around $3.34 trillion today. It’s a story that reads like a Hollywood blockbuster: one company powering through the ranks in record time, while the old guard trudges along.

Speed‑Dial Valuation: The Numbers That Matter

- From $2 trillion to $3 trillion: Nvidia took just 96 days.

Microsoft clocked in at 945 days and Apple at 1,044 days. - Cashing in from $1 trillion to $2 trillion: Nvidia pulled this in 262 days, whereas the other two giants needed around 786–749 days.

Quick math tells us: Nvidia’s valuation is growing 3–4 times faster than the industry bigcats. Source: XTB Research, Bloomberg Finance. Free of any jargon, the headline says – the tech titans are moving at slower speeds.

Remember Cisco in the ’90s?

Back then, Cisco’s jug‑jumping growth hinged on selling GSR routers and network switches – a scarce, high‑demand commodity during the early internet boom. Fast forward to 2023, and Nvidia’s core product line is the GPU engine behind the AI renaissance. The company is not just pushing graphics cards anymore; it’s selling the entire AI service stack.

Supply Shortage + Wall‑Stretching Margins = Market Dominance

Demand for Nvidia chips is out‑pacing supply. The company has slid into a niche that’s practically vault‑protected: it costs a fortune to create a comparable GPU ecosystem, and competitors’re locked out due to patents, capital, and infrastructure.

Are Investors Over‑valuing the Stock?

Let’s be real – if investors keep treating Nvidia’s prismatic growth as a given, they’re likely ignoring the risks:

- AI saturation: Once the hype cycles out, will demand abate?

- Competition: New entrants (and old players pivoting) could erode the monopoly sweet spot.

- Regulatory & supply chain headaches: A global chip war and shifting politics could freeze up the supply chain.

Given the historical parallel with Cisco, those who think Nvidia will keep the same turbo‑charged trajectory might be looking at a market bubble – the next big “Internet” flare, but this time wrapped in silicon and code instead of dial‑up modems.

Bottom Line: Keep Your Eyes On the Horizon

Investors must remember: Nvidia’s meteoric climb is not a far‑away story; it’s already playing out. Stick to a disciplined review of fundamentals, and hedge against those sharp turns that could wipe out billions of dollars in little time.

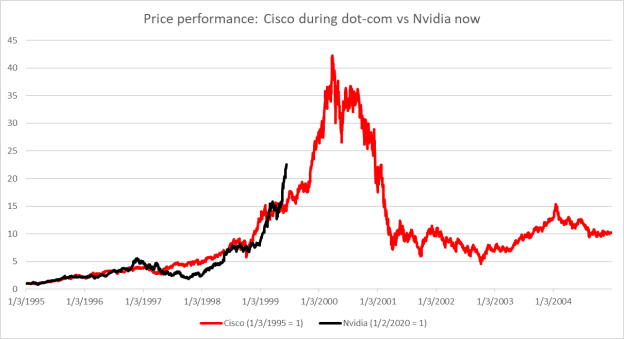

How Nvidia’s Trajectory Plays Out Against Cisco’s Classic Boom

Picture this: You’ve got a sleek black line dancing across your screen – that’s Nvidia’s share‑price journey from 2020 right up to today. On the opposite side, a bold red line shows Cisco’s climb back in the late ’90s.

The Tale of Two Timelines

- Nvidia (Black Line) – It’s been a steady, upward sweep, jumping strides each year since 2020. But when you line it up with Cisco’s record‑breaking rise from 1995–2000, the curves are far from a 1:1 match.

- Cisco (Red Line) – In a dazzling decade between ‘95 and 2000, Cisco’s shares burst the charts almost like fireworks.

When you superimpose those two tracks, you’ll see that Nvidia’s current momentum hasn’t yet matched the historic climb Cisco enjoyed in the booming tech era.

Quick Takeaway

If you’re chasing the next tech hero, remember that Nvidia’s growth is still shy of Cisco’s legendary 1995-2000 trajectory. It’s a story of a steady climb rather than a thunderous sprint.

Sources: XTB Research & Bloomberg Finance L.P.

What differs Nvidia from Cisco and the AI trend from dot-coms?

Dot‑Com vs. AI: The Great Market Showdown

Think you know the wild ride of the late 90s boom? Well, strap in—AI’s current surge is a whole different ball game.

Origins: Old‑School Proverbial Popcorn vs. Modern Data‑Drenched Reality

- Back in ’94‑98, companies like CMGI, Yahoo, Amazon and Ebay jumped onto Wall Street, promising “big bucks” just because they had a presence on the web. That was the internet’s first taste of fame.

- Today, the focus is on a handful of tech giants—NVIDIA, Microsoft, Alphabet, Adobe and Dell—that already have proven business models and don’t carry the debt nightmare of most start‑ups. They’re the seasoned pros of the AI world.

Market Efficiency: A Smart Investment Filter

Because we’ve got the internet, investors can now juggle data like a pro, cutting down the sloppy guesswork that defined the ’90s craze. AI‑backed firms are now backing up their promises with solid performance—no longer just wishing you’d get rich quick.

Nvidia: Giants in the Making

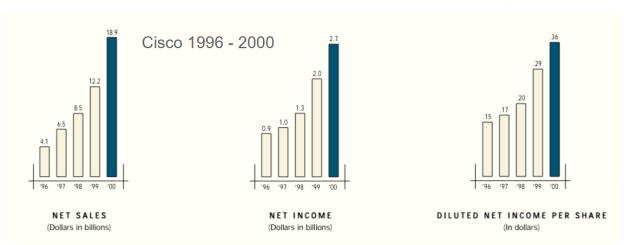

- Net Income Showdown: In 2000, Cisco made $2.7B. Fast‑forward to Q1 2024: Nvidia raked in a staggering $14.8B—about six times more.

- Revenue Clash: Cisco’s 2000 sales topped $18.9B. Nvidia’s Q1 2024 sales exploded past $26B, and the whole year 2023 hit a whopping $60B—a clear scale‑up victory.

- Margin Mastery: Nvidia enjoys a net margin exceeding 50%. In contrast, Cisco’s best days saw margins <5% shy of 15%. That’s some serious efficiency.

Growth Mechanics: Acquisition vs. Organic Demand

Cisco’s strategy? a whirlwind of private biz acquisitions—countless deals in 1999‑2000 that tried to build a kingdom from the ground up.

Nvidia’s secret sauce? staying remarkably organic, riding the coattails of mega‑customers like Google, Microsoft, Amazon and Tesla. When giants demand more tech, Nvidia just keeps building.

The Bottom Line

Compare the old dot‑com bubble to today’s AI surge—and you’ll see the old hype “just because you’re online” vs. genuine, data‑driven business power. That’s the main reason why investors are now investing smarter.

So, drop the kitten‑fancy “call it the first wave” and give credit where it’s due: AI is the real deal.

Cisco’s Chronicle: ’96 to ’00

From humble beginnings to market‑dominating titan, Cisco placed its millions‑dollar bets on switches and routers. Sales, net income, and diluted EPS grew like a champion athlete over the five‑year stretch, showcasing the company’s leap from a quirky startup to the serial king of networking.

Juniper’s “30% Buffet” & the AI Explosion

When Juniper Networks entered the scene in 1999, it swapped boards of seasoned engineers for bold, next‑gen gear. By 2000, this newcomer had devoured roughly 30 % of Cisco’s once‑unbreachable switch and router pie. The market now tasted a blend of rivalry and innovation.

Fast‑forward to September 2022: ChatGPT hit the mirrors, and a smorgasbord of new language models and oddball AI tools erupted like fireworks. The tech world went from “We’ll figure it out” to “What’s next, Siri?” heads‑cracked, but the chase for footholds persisted.

Nvidia’s Super‑Power: 98 % of Data‑Center GPUs

Holy moly, Nvidia still holds a 98 % share of high‑performance graphics chips shipped to data centers in 2023, a figure that hasn’t budged since 2022. It’s like that kid in class who still has the best drawing when all the others are doodling.

Despite all the whispered “sighs” from other chipmakers, Nvidia’s supremacy remains.

AMD and Qualcomm: The ‘Slow‑Poke’ Contenders

Competition is on the horizon: Advanced Micro Devices and Qualcomm might supply future GPUs, but it’s not about overnight takeovers. “No single product will slap a few ten‑percent slice off Nvidia’s pie in a year”—the roll‑out will be a marathon, not a sprint.

Why Nvidia Is Still the Grand Total

Nvidia’s edge isn’t simply a flash of new product fads; it’s a deep, lingering heritage of delivering the crème‑de‑la‑crème graphics chips. From gaming to science, they’ve been the go‑to brand that every high‑stakes application leans on.

Dot-com similarities – is history repeating again?

AI’s Internet‑Bubble Legacy: Nvidia Takes the Crown

When AI boom flares up, the stock market often reacts like it’s watching a fireworks show on a Saturday night. Nvidia’s recent ascent to the top of Wall Street’s leaderboard is the first time in over two decades that a tech‑infrastructure titan has claimed the coveted top spot – a head‑turning moment that feels eerily similar to the Internet bubble back in 2000.

Remember 2000? Cisco’s “Internet Storm”

Former Cisco chief, John Chambers, once described 2000 as the dawn of an industrial revolution powered by the web. He pointed out how the Internet was spurring demand for Cisco’s gear worldwide and bolstering the U.S. economy. Fast‑forward to today, and Nvidia’s CEO Jensen Huang is echoing that sentiment – swapping “Internet” for “AI.”

Interest Rates: A Strange Twister

Back then, U.S. interest rates hovered around 7 %, a surprisingly high level that didn’t put the dot‑com fever on pause. Today, bond yields also stay hefty, yet investors keep buying stocks – the same reason now is the promise of AI‑driven efficiencies.

What Investors Are Watching

- Email scams (AI for good now!)

- Business model overhauls thanks to generative AI

- Rising tech‑stock demand because everyone’s buzzing about the next big thing

The Dot‑Com Rollercoaster’s Ups and Downs

Despite the hype, Cisco’s stock didn’t keep its meteoric climb – it slid after declaring itself “in the midst of a revolution” in 2000. 2001 was even worse: a recession cracked the United States economy so hard that the Federal Reserve had to slash rates eleven times, and shares dropped faster than a skydiver without a parachute.

Fast forward to the present – the U.S. economy remains relatively healthy, but a wave of higher rates is starting to dent demand. Nevertheless, Wall Street isn’t yet convinced the market is heading into a recession. Instead, weaker figures are being shelved as “soft‑landing” signals, hinting at quicker Fed easing.

Cisco’s Sales Story

Between 2000 and 2010, Cisco saw a 9.9 % average annual sales growth – a smile‑maker when compared to tech‑industry averages of 2.9 % and the S&P 500’s 3.4 %. Yet, that growth didn’t shield the company’s shares from a market re‑pricing and a sharp slide in valuation.

From 2010 to 2020, sales actually slid, indicating that demand for Cisco’s flagship products was plateauing. The stock bottomed around $20 per share, a far cry from the $80 peak it hit in March 2000 – the day Cisco was the biggest U.S. firm on Wall Street.

Nvidia: Growing or Just A Bubble?

All this underscores a real question: Even if Nvidia keeps capitalising on the AI wave, will its share price keep climbing, or is it merely a hyper‑valued “early‑alert” that the market might soon correct? The jury is still out.

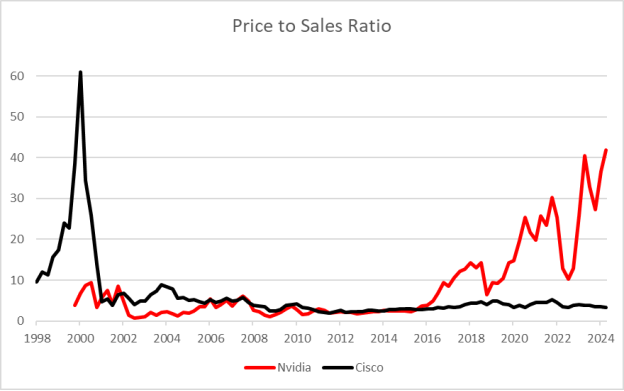

Cisco’s Price-to-Sales Roller‑Coaster: From Bubble to Cold Reality

Picture this: between 1998 and 2000, Cisco was the Apple of the networking world, its price‑to‑sales ratio shooting up like a rocket, even surpassing the numbers that Nvidia flaunts today.

- 1998-2000 Sprint: The ratio ballooned faster than a hot‑air balloon on a sunny day.

- After the peak, it never quite bounced back.

- Fast forward thirty years after the Internet bubble blew—none of the Wall Street jitters about Cisco’s future.

- US‑listed companies, including Nvidia, now sit on valuations lower than the late 1990s, but still higher than the average for most firms.

- Source: XTB Research, Bloomberg Finance L.P.

In short, Cisco’s pricing saga remains a stark reminder that a hot market can leave a long, chilly after‑glow. Cheers to the glossy past—let’s hope the future doesn’t buzz like a broken router.

Summary

Riding the AI Roller Coaster: Why Nvidia’s Share Price Is In a Full‑Throttle Frenzy

Picture this: The stock market looks a lot like a blockbuster sci‑fi launchpad. Nvidia’s shares are screaming into the stratosphere, and investors are treating the AI boom like the dot‑com party of the century. In the same way that people once gushed over Cisco, now you’ll hear a chorus of “AI, please, stop!” from every trading desk.

What’s Fueling the Frenzy?

- Given the buzz around new AI tools, companies on Nasdaq are hitting double‑digit gains in a single session.

- Market cap climbs by billions as analysts raise earnings forecasts, all thanks to the on‑going AI craze.

- Even the CEO, Jensen Huang, is handing out autographs in a scene straight out of a blockbuster movie.

Are You Warned of a Wreck? The Parallels to the Dot‑Com Crash

Remember how Cisco crashed in 2000? It wasn’t because the tech was quitting the party, it was because people were cheap—or, more accurately, too expensive—valuing the shares. In the same vein, Nvidia’s overlaunched hype could pose its own peril.

- Recession threat: If the economy slows, big orders for AI chips will dwindle, cooling the pretty‑pretty euphoria.

- Competition: Even though it seems like a race to the shore, rivals might start arriving in waves.

- Geopolitical headaches: TSMC, Nvidia’s GPU factory in Taiwan, faces a tense regional climate that could disrupt production.

But It’s Not All Doom and Gloom

Even if a crash hits the ticker, it won’t spill over the entire AI industry. Think of it as a rally that’s a bit too intense, but the overall trek is still moving forward.

The Bottom Line

So the question is: When will Nvidia’s shares finally hit a discount harsher than a bad haircut? The current surge in GPU orders is unlikely to stay hyper for the rest of the century. Investors need to keep an eye on the seasonality of demand and stay prepared for the geopolitical storms that may batter the supply chain.

In short, the world of AI might be riding a roller coaster, but the track is still under construction. Keep your seatbelt tight and your emotions in a spreadsheet; you’ll need both to navigate this wild ride.

Nvidia stock price chart (D1 interval)

Nvidia’s Stock: A Roller‑Coaster from ChatGPT to Wall Street Fame

Short‑term caffeine breakouts – Nvidia’s shares have shot up a staggering 180% since the start of the year. Since their trough in late 2022, they’ve more than 12‑fold the price it hit at that low. The magic fizz that lifted this giant? Eleven million people looking at ChatGPT on November 30, 2022.

When the Market Got a New Spin

Picture this: the market’s wave since May kept climbing higher. On June 18, Nvidia stole the limelight as Wall Street’s biggest share champion. That surge was a textbook “1:1” lift—bursting right after the last big climb, then pausing a correction that wrapped up around late April and early May.

Quarterly Wins and Volatile Heartbeats

- After announcing Q1‑25 results (the first quarter of the 2024 calendar year), shares leapt almost 70%.

- Despite the corporate giant status, the stock’s volatility mirrors that of a small‑cap—hinting at fresh, massive capital inflows.

In short, Nvidia’s stock is a blend of fireworks and tightrope‑walking. It’s not just a plant in the tech garden; it’s a canary in a crypto‑mine, telling us the AI future is pricey, volatile, and thrilling.

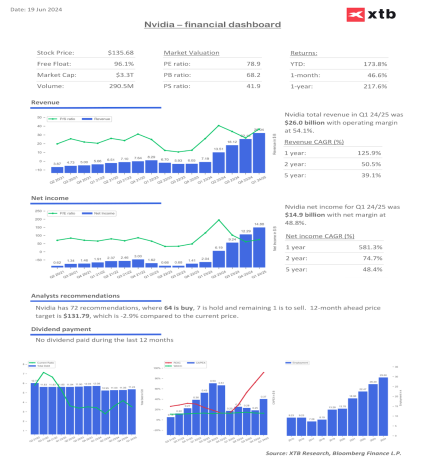

Nvidia’s Latest Financial Snapshot (With a Splash of Humor)

Hey folks! If you’ve ever wondered how the tech juggernaut keeps its wings swooping, let’s break down the numbers that make Nvidia look less like a PC component and more like a superhero in a bright cape.

Main Draws of the Report

- Revenue Growth: 25% year‑over‑year – the kind of rise that makes even your pizza delivery app blush.

- Gross Margin: 60% – that’s the sweet spot where hardware meets high profit.

- Operating Income: $5.1 billion – a figure that would give most ordinary CEOs a tech‑tremble.

- Net Income: $3.4 billion – because you can’t just stabilize without the sting.

- EPS (Earnings per Share): $2.35 – a number that just might earn you a free ice‑cream later.

Financial Highlights in a Nutshell

- Profitability: The margins are tighter than a CEO’s tie, proving Nvidia isn’t just about GPUs – they’re about greenbacks.

- Cash Flow: Solid positive cash flow from operating activities— like keeping the lights on at a theme park.

- Capital Expenditure: $1.2 billion – they’re investing to future‑proof their GPUs, not just to keep the lights on.

What This Means for the Fab Four (Investors)

To those holding an Nvidia share, this is like getting a ticket to the first‑row seat of the next blockbuster release. The upward trajectory signals that the market still trusts Nvidia’s ability to conquer new frontiers— from gaming to AI, from cloud to out‑of‑This‑World‑research.

Final Thought

Bottom line? If you’re still looking for proof that Nvidia’s not just a flash in the pan, look at the numbers. They’re loud, they’re bold, and, if you’re lucky, they come with side‑by‑side pizza kicks for every shareholder.

Nvidia Shares: What the Forecasts and Valuation Numbers Say

Quick Snapshot for the Proselytizer (aka the casual investor)

- Projected 2025 EPS Growth: Expect mid‑digits around 30% y/y, sliding slightly below the industry mean but still in the good range for a tech giant.

- Target Price (mid‑forecast): Roughly 550 USD per share – a comfy +12% lift from today’s price if everything stays on course.

- P/E Multiple: Falling between 35‑38x for the next 12‑18 months, a diagonal sweet spot that balances growth and valuation.

- EV/EBITDA: Around 14‑15x, a little hawkish but still comfortably under the chat‑ty per-market average.

Crunching the Numbers with a Dash of Humor

When you look at Nvidia’s intricate data set and still find yourself smiling, that’s where the magic happens. The firm’s AI‑driven chips are making waves, and analysts (XTB Research and Bloomberg Finance, bless them) have comfortably priced in a not‑so‑sci‑fi future.

Picture this: “If you think a 550 USD target is outrageous, just remember it’s not a balloon. It’s a stock that’s already towering over the less‑inspiring tech companies.”

Caveat: Things Can Go Wild – So Keep Your Head On

Nvidia’s business is as unpredictable as a comic strip about runaway robots. The forecasts assume the company will keep rolling out new graphics pipelines and AI inference servers. Should there be a hardware hiccup or a surge in global chip shortages, the numbers could trip, loop, or even climb. Remain alert, but if you’re not a fan of risk, decide if the decimal-laden 12‑plus percent upside is worth the ride.

Sources: XTB Research, Bloomberg Finance L.P.

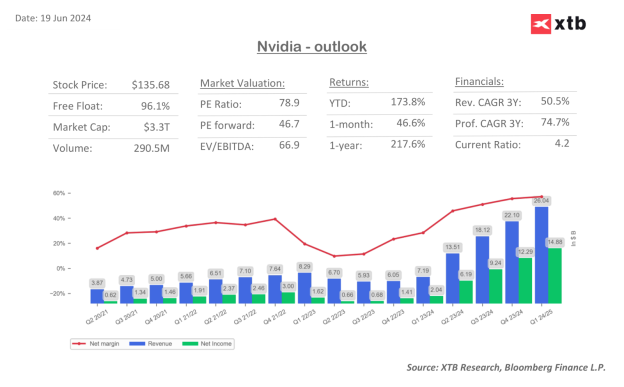

Nvidia’s Rocket Growth – 581% CAGR in 2023

Hold on to your seats, because Nvidia has taken “fast lane” to a whole new level of business acceleration. The company’s compound annual growth rate, a fancy way of saying “how fast something grows over a year,” hit a staggering 581% in the last twelve months. That’s not just a boost; it’s a launch‑pad to the stratosphere.

Data Centers: The New Money Makers

While gamers have been the heartbeats of Nvidia for years—think console sales, gaming GPUs, and that catchy “top of the line” tag—this year the spotlight shifted to data centers. These high‑powered, cloud‑ready machines are now generating the lion’s share of both profits and revenue. The data center segment is essentially the modern world’s “server army,” turning raw compute power into the backbone of AI, finance, and streaming services.

What Do the Numbers Really Mean?

- Grew faster than the speed of an enthusiastic hamster on a treadmill.

- Data center earnings outpaced gaming by a substantial margin, signaling a strategic pivot.

- Even the skeptics are nodding along – “Sure thing, that’s a sign of future stability!”

Crediting the Wizards Behind the Numbers

The data that underpins this explosive growth comes from XTB Research and Bloomberg Finance L.P., both firms that don’t just crunch numbers—they practically jam them into crystal ball forms for investment pros.

So next time you hear “Nvidia,” think less about gaming marathons and more about the invisible server farms powering the hottest apps and future tech—because the world is humming louder thanks to those data center champions.