Job Market Soars—or Not? A Quick Look at April US Employment Stats

April’s labor report is a mixed bag: payroll growth wobbles below the hype, unemployment ticks up, and wages are finally taking a breather.

What the Numbers Really Mean

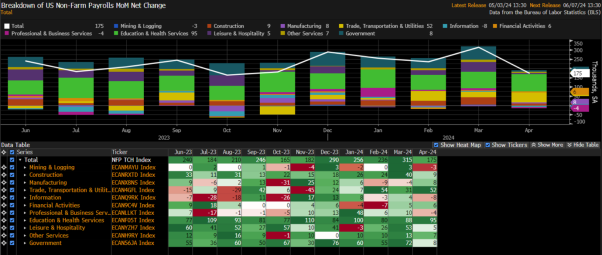

- Nonfarm payrolls jumped 175k—a little shy of the 240k consensus, but comfortably inside the predicted range of 145k‑280k.

- Off the beaten track: February and March job figures were trimmed by 22k in total, pulling the 3‑month average down to 242k.

- This 242k is roughly spot‑on with what the market says is needed to keep hires in line with the ever‑growing workforce.

Why We’re Not Raising the Alarm

Despite the “cooling” label, economists are holding their breath. The market’s response has stayed mellow, and the Fed’s policy dial is still set to “no action for now.” In other words, the economy is getting a gentle chill, not a frosty shock.

The Bottom Line

Jobs are growing—just not as big‑time as some had hoped—wages are easing, and unemployment is inching up. All told, it’s a quieter day in the labor market, but taps on the policy table are staying muted.

What the Numbers Are Saying About the US Workforce

Pull the payrolls print like a secret recipe, and you’ll see that the job scene is more uneven than a toddler’s art project. Some categories are popping off like fireworks, while others are putting on a sad karaoke set.

Top‑Dogs of the Month

- Education & Health – these two were the big losers in the job‑gain lottery, bringing in the highest monthly additions with a polite “hello” to more teachers, nurses, and all the folks making the world a healthier place.

- Mining & Logging – folks dusted off their pickaxes only to find the mine had less excitement this month, leading to a gentle decline in jobs.

- Information, Professional, and Business Services – they tried to breakdance in the career dancefloor, but ended up stepping off, causing mild declines in hires.

Why This Matters—and Why You Should Care

Even if the headlines say everything’s fine, the data tells a whacky story of some sectors sprinting while others are doing the slow shuffle. Dive in, and you’ll learn that the world of work is as unpredictable as your favorite streaming playlist.

Next Steps

Keep an eye on those education and health booms – they’re literally the good news amid a mid‑season slump. And for the mining and professional folks? It’s time to roll up your sleeves (or your logging boots) and chase the next job sprint!

Take a Peek at April’s Pay‑Rise Scoop

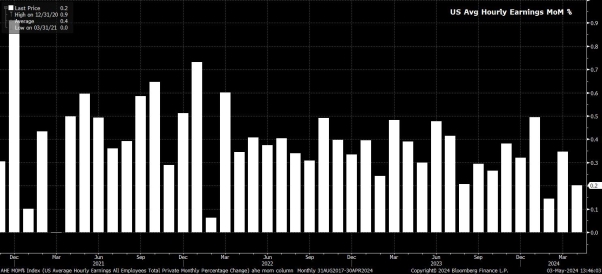

So, what’s the buzz this month? Average hourly earnings ticked up 0.2%. A modest nudge, but it’s a bit cooler than the money‑lenses were expecting it to hold steady from the 0.3% rise seen in March.

Year‑on‑Year: The Slow‑Moody Trend

- Annual earnings climbed 3.9% compared to last year – a dip from the 4.1% March bump.

- That’s still in the ballpark of the Fed’s sweet spot of a 2% inflation target, but it looks like the money trickles a touch more slowly.

- Why the slowdown? Two things: a gentler month‑to‑month lift and the fact that 2023’s earnings data are still high‑fived into the mix.

Hours: A Small Every‑Day Shake‑Up

And in the “how long are people working?” corner, the average hours dipped just a hair from 34.4 to 34.3. Maybe people are taking a tiny breather, or just squeezing the clock a bit tighter.

All told, April’s earnings story is a gentle, steady‑pace dance – not a sprint, not a marathon, just a calm jog toward keeping real pay growth in line with what the Fed’s goal on inflation looks like. Keep your ears open; next month might bring a new twist to the payroll plot!

Labour Market Snapshot

Hold onto your hats, because unemployment was at 3.9% last month—a smidge over the 3.8% yardstick people had in mind. Guess what? The market still feels like a locked door; folks are hustling hard.

- Job Participation: 62.7% of people are looking – that’s the solid majority staying in the game.

- Underemployment: up just a bit to 7.4% (from 7.3%): a tiny shift, but still a reminder that many can’t land the full-time gig they want.

All the bits and bobs point to a labor arena that’s tighter than a drum – people serious about catching a job, but the job landscape is still a bit soccer‑ball of a challenge.

Fed Policy Outlook Tweaks After Softer Payrolls

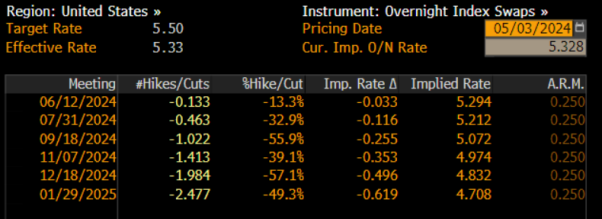

When the latest job data came in a bit more chill than we thought, the market politely adjusted its expectations for the Fed’s upcoming moves. The shift was pretty steep, but most of it came from the old-school “hawkish” view that had taken hold before the payroll numbers dropped. So, when the market finally caught the new info, positions began to unwind.

In practical terms, the USD Overnight Index Swap (OIS) curve now expects just over 50 basis points of easing this year – that’s two rate cuts – compared to roughly 43 basis points before the payroll release. The curve has also lined up the first 25‑basis‑point cut for this September FOMC meeting (instead of the earlier November guess).

This pricing is more in line with Chair Powell’s latest stance, who reminded us that a “couple of tenths” jump in unemployment alone wouldn’t justify a rate cut or signal a sudden labor‑market weakness. In other words, the Fed isn’t about to pan out just because the job numbers slipped a little.

What Happened After the Payrolls Print

Guess what? Even though the numbers came out, the market still had a feeling of calm – a dovish vibe that spread like a chill breeze across every corner.

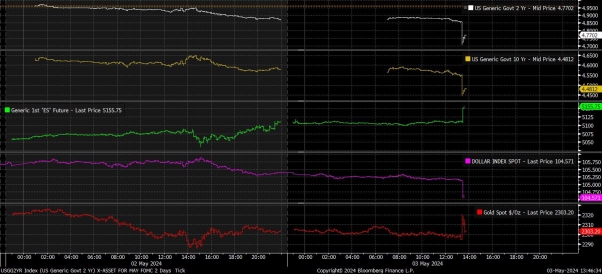

The Treasury Tango

So, what happened next? The Treasury side of things went on a runaway spree. Short‐dated bonds, the front‑end of the curve, hugged the market hard. 2‑year notes fell as much as 15 basis points all day – and then, later, little‑bit. This sudden slide sent the greenback back below that big 105 mark, which in turn bumped the DXY and USD/JPY dancing off their old 152‑level stances.

Good News for Japan

Hold up, the yen folks – the Japanese Ministry of Finance – had one thumbs‑up here. The USD/JPY dipping below 152 is a pretty sweet win for anyone working to curb yen weakness.

Gold’s Glittering Comeback

- Lower yields gave the precious metal a boost.

- Gold shot up to about $2,300 per ounce, feeling like it finally found its rhythm.

Stocks—Yes, They’re Up!

- Front‑end S&P and Nasdaq futures surged more than 1% over the print.

- By the end, equity markets were in a good vibe, underscoring how confident folks are about the short‑term market outlook.

So, there you go. It’s a gentle market reset with a cool‑down in the Treasury, a steady heartbeat in the stocks, and a shiny moment for the gold, all while the yen gets a friendly nudge back to a stronger spot.

What the April Jobs Beat Means for the Fed—and for Your Wallet

Short version: The jobs data didn’t shout “Boom, cut!” to the market. The real kicker is inflation, not employment. The Fed still looks set to trim rates, and that’ll keep risk assets looking pretty good. The dollar? It’s stuck in a plateau—won’t hop up again anytime soon.

Why the Jobs Report Fell Short of a Shockwave

The paycheck numbers gave folks a gentle nudge toward a dovish mood, but the Fed is eyeing the bigger picture. Inflation is the heartbeat that will dictate when the first rate cut lands. So, keep an eye on the CPI release on May 15—if prices are still dancing around or wobbling, that’s the risk event that markets will wrestle with.

Labour Market: Cooling, But Not Shivering

There’s a hint, a faint whisper, that the labour market is easing off a bit—think of it as the economy’s first sigh of relief. Still, this cooling is far from a full-on do‑you‑see‑it scenario. It isn’t enough to trigger a policy change right now.

Fed’s Likely Next Move

- Rate cuts are the probable next step, if not inevitable.

- The FOMC’s mantra: Reduce the restrictive vibe ASAP.

- With these moves, risk assets remain on the throne, backed by the “Fed Put” concept—so investors can keep riding that risk curve.

The Dollar: Stuck in a Plateau

Expect the USD to stay mid‑level. Markets are comfortable with 1‑2 cuts this year, setting a high bar for further short‑term appreciation. Think of it as the dollar taking a break on a patio—no coffee yet.

Bottom Line for Your Portfolio

— Keep an eye on inflation data for the big news.

— A Fed rate cut is almost on the horizon; be ready for a boost in risk‑seeking.

— The dollar’s climb has halted; expect it to hover for now.