March 2025 US Job Numbers: A Stunning Surprise

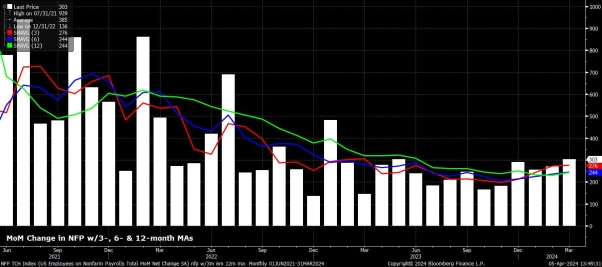

What a whirlwind we’ve had in March folks— the Bureau of Labor Statistics decided to throw a big surprise party for the economy: 303,000 new jobs added in the month alone. That is a blast of a number, smashing the expected +214,000 and even topping the high end of the forecast range.

Why This Isn’t a Policy Game‑Changer

- Inflation remains the central theme for the Federal Open Market Committee (FOMC).

- Despite the job boom, the Fed is playing it cool— patient and data‑dependent, not rushing to tighten or loosen locks.

- The jobs data gives a thumbs‑up to that patient stance but doesn’t shift the policy dial significantly.

Three‑Month Snapshot: Year‑High Growth

- January & February prints were nudged upward by a total +22,000— a positive tweak to the feel of the economy.

- When you combine the March spike, the revised Jan/Feb numbers stack up to a +276,000 average growth over three months.

- This average sits at the highest level in a whole year— a golden touch‑point for labor market analysts.

Bottom line? Employment is flexing its muscles, but the Fed stays on its cool‑down track, keeping eyes on inflation. Let’s watch how the job story unfolds while the central bank balances that delicate act of monetary restraint.

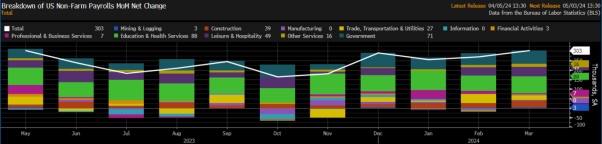

What the Numbers Really Say

When you look at the raw hire data, the story is louder than the headline might suggest.

Everything but a Couple of Sectors Is on the Rise

- Every industry added jobs this month.

- Only manufacturing and information technology held steady—no net gains there.

Which Sectors Brought the Biggest Boost?

The government was the star of the show, followed closely by the leisure and hospitality sectors.

Bottom Line: A Strong Plus in the NFP Print

Overall, the Non‑Farm Payroll figures keep the economy moving forward, with a clear shift in hiring toward public services and “fun‑filled” areas.

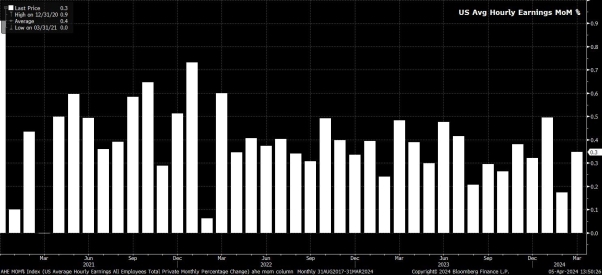

Wage Whisper: The March Earnings Scoop

Did Folks Just Get A Tiny Pay Boost?

In plain English, average hourly earnings bumped up a modest 0.3% in March—slightly nicer than the almost‑flat 0.1% in February.

Year‑Over‑Year: A Hint of Chill

When we look a year ahead, wages slid to 4.1% growth from the 4.3% seen just a month ago, thanks mainly to higher comparables last year making the pace look a touch cooler.

Work Hours: A Tiny Tweak

And the average workweek ticked up just a smidge—to 34.4 hours from 34.3, basically the same grind.

- MoM earnings rise: 0.3% (March) vs. 0.1% (Feb)

- YoY earnings rise: 4.1% (March) vs. 4.3% (Feb)

- Avg. weekly hours: 34.4 (March) vs. 34.3 (Feb)

Bottom line: wages grew a little, the annual momentum cooled, and the hustles per week stay almost steady—no wild spikes, just a calm, consistent roll.

Labor Market Snapshot: Slipping Unemployment, Steady Gains and a Bit of Relatable Lightness

Last month’s headline figure for unemployment quietly slipped to 3.8%, a gentle step down from the 3.9% seen in February. That 3.9% figure had already been the highest since 2022 kicked off, so the dip is more of a small‑town joke than a headline‑shocking plummet.

Underemployment Remains a Steady Stone

Looking beyond the headline, underemployment was stubbornly unchanged at 7.3%. It’s like that one family dog who refuses to shed any fur—even when you want a clean house.

Participation: Slowly Climbing Back to Hometown Heights

Workforce participation nudged up by 0.2 percentage points to 62.7%. That’s a tidy gain, inching us back toward the “cycle highs” that fans earlier this year have been chasing. Think of it as the workforce steadily gathering its sneakers and gearing up to hit the town’s monthly marathon.

- Headline unemployment: 3.8% (slightly lower than 3.9% February)

- Underemployment: 7.3% (steady)

- Participation: 62.7% (up 0.2pp)

All told, the U.S. labor market is still holding a tight grip, but the slight upticks in participation and the quiet dip in unemployment give us a breather to celebrate—in the good sense, of course. Cheers to a market that’s staying folks within the loop and making sure the job ribwith isn’t just a rumor.

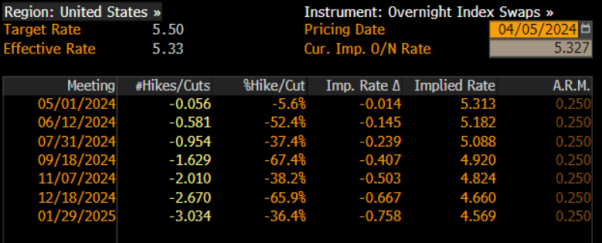

Why Jobs Won’t Shake Up the FED’s Rate‑Cut Plan

Even after a roaring job report, the Federal Open Market Committee (FOMC) is pretty certain that the policy track won’t turn on its head. As Chair Powell reminded everyone in March, a hot labor market doesn’t mean we should pause on cutting rates.

Key Takeaways

- Strong jobs → keep cutting? Yes—no sign that inflation worries will derail the plan.

- Market reaction to the latest payrolls? Minimally shaken.

- The USD Overnight Index Swap (OIS) market stays laser‑focused on a 25‑basis‑point dip in July.

- Year‑end easing is pegged around 68 basis points, slightly softer than the 71 bp expected before the release.

What the Numbers Say

The pricing for the first Fed cut is still on track for July, but the overall climb to year‑end is a touch less aggressive—just a pinch of hawkish repricing.

Bottom Line

In short: the toughest portion of the job market doesn’t change the Fed’s current mindset. Rate cuts remain on the cards, and the markets reflect that more or less as expected. No dramatic pivots, just steady, predictable moves—like a well‑brewed cup of coffee, not a crash‑test scenario.

Market’s Sober Stance After the Jobs Report

Just like a quiet Sunday afternoon after a concert, the market’s reaction to the latest jobs data was surprisingly calm. Even though the numbers hit a few low points—stocks sagged to daily lows, Treasury yields spiked, and the dollar ripped through the day’s resistance—the moves were short and sweet.

Brief Sprint, Then a Relaxed Chill

- Equities dipped to their lowest since Monday’s morning rush.

- Treasuries pushed the day’s yields higher, with the front‑end leading the pack.

- The dollar broke the previous highs, shining like a sunrise over Wall Street.

But like a sudden breeze, the impact blew away fast—everything bounced back to its pre‑report levels in no time. Investors merely take a quick glance, then return to their usual rhythm.

Risk‑Landscape Remains Mostly the Same

In the grand scheme, the jobs report hasn’t shaken the market’s risk equilibrium. The most likely path still tips in favor of risk‑seeking assets: the “Fed Put” (the cushion for higher rates) remains active, and investors anticipate that rate cuts will probably start around summer. Simultaneously, the dollar is nudged slightly upward, because the U.S. labor market’s resilience touches the G10 FX story of “U.S. exceptionalism”.

Policy Outlook: Inflation Still Reigns

While the two elements of the Fed’s dual mandate—price stability and maximum employment—seem to be balancing each other better now, inflation remains the king of the jungle when it comes to determining the FOMC’s cutting timeline and magnitude. The next CPI eye‑opener on April 10th will be a key turning point, especially after three consecutive headline figures that kept the heat meter well above expectations.

So, if you want a glimpse of what the markets might look like next week, keep your eyes on the CPI. Until then, the present market vibe is to ride out the calm—low volatility, steady dollar, and a hint that risk assets could still keep finding sunshine.