March MPC Meeting: A Strategic Pause for the Bank of England

Think of this month’s meeting as a polite queue at the bank rather than a full‑blown policy overhaul. The Bank of England’s Monetary Policy Committee (MPC) is holding the line for now, keeping the Bank Rate steady at 5.25%.

Why the Delay?

- Inflation on Watch: Policymakers are waiting to confirm that inflation is easing toward the 2% goal.

- Data‑Driven Decisions: They prefer more evidence before making any cuts.

- “Table Mountain” Approach: “Old Lady” Chief Economist Pill described this cautious stance as scaling a steep cliff rather than leaping off a cliff.

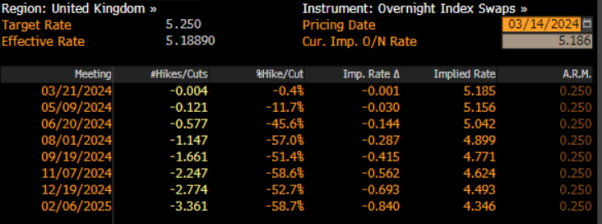

What the Markets Say

The GBP OIS curve tells a clear story: there’s no movement expected today. Money markets are split—about 50/50 odds for a 25 basis point cut in June and can fully price that cut into August.

Bottom line: No surprises this month. The MPC is tightening its calm, keeping the policy status quo while waiting for the next solid data beat.

Why the MPC’s Vote Might Be a Three‑Way Tug‑of‑War

Picture the March Monetary Policy Committee like a crowded coffee shop, where the barista (the MPC) must decide whether to add more sugar (raise rates) or cut back on caffeine (lower rates). The last meeting flipped the script, with a 3‑way split that’s the most dramatic vote division in 15 years.

Who Cast Which Ballot?

- Dubutura Dhingra (the smooth‑talking, “forever‑dove” of the committee) went all‑in for a 25‑basis‑point cut. “Things are cooling,” he says. Inflation looks ready to dip, so maybe we should loosen the reins a bit.

- Sir Haskel & Mr. Mann (the real‑talking hawks) preferred to hike by another 25 bp. “Inflation’s stubborn,” they warn. They’re not willing to put the pedal down on even a single notch without clearer evidence.

So, the committee is stuck between a tempting salt‑and‑pepper pizza of cuts and hikes. Will the party line shift? Likely, but only if the hawks decide to swing in favor of the majority.

Policy Guidance: The Same Old Playbook

The MPC’s note to the public isn’t about changing the game entirely. The language will likely stay the “restrict the policy for a while longer” groove, keeping the eye on that 2% inflation target. “We’re still watching,” they’ll say, letting us know that the high‑stakes stopwatch is still ticking.

Current Market Forecasts: Almost Three Cuts in 2025

Despite the murky vote, the MPC seems to be riding the wave of market expectations. With a trio of 25‑bp cuts in place, the forecast suggests a production‑line of easing that’s happening on autopilot. The February inflation projections, assuming a flat 5% policy rate, hint that we’ll still be short of the 2% sweet spot, pushing the board to inch toward cuts down the road.

Bottom Line?

Call it a seesaw: the MPC is juggling, with the dovish side leaning toward easing and the hawkish side staying firm. Meanwhile, the guidance stays sweetly consistent, and the market’s already humming in sync with a chain of cuts that might just bleed the inflation target down to the desired spot.

Will the Money Miracle Arrive? A Quick Look at Tomorrow’s Inflation Numbers

Hold onto your wallets, because the February inflation data isn’t up on the screen yet. It’s slated to drop on March 20th, the very day the Monetary Policy Committee (MPC) sits down for its meeting. Picture this: the MPC votes in the late‑night wiggle‑tim, and the public only sees the official announcement the next morning.

What’s the Buzz About?

- Headline & Core Inflation: Both are expected to keep slowing – a nice, gentle descent.

- But guess what? They’ll still be sky‑high above the Bank of England’s golden goal of 2 %.

- The real drama will center on services inflation, which is still dancing north of 6 % and looking like it’s stuck in a sticky jam.

Why Services Matter

Policymakers have their eyes glued to this metric. Services prices are stubborn, refusing to drop, and they’re the big tease the Bank keeps in mind when deciding the next rate move.

Can We Hit the 2 % Target?

The good news—lazy bone: the 2 % inflation target is almost sure to hit in the spring. That could very well happen fresh and bright by the June MPC meeting. How?

- There’s a big drop in the energy price cap, which is like trimming the bulk of the inflation barometer.

- Plus, the March budget froze some fuel & alcohol duties, shaving about 0.2 pp off headline inflation for the rest of the year.

So, while the numbers haven’t landed yet, the story looks promising: slower rates, a bit of easing from energy, and a budget freeze that does a smidge of good. Let’s keep an eye on those services inflation spikes—if they bounce, the party may be postponed.

Will the 2% Inflation Target Dance Away?

Even though the Bank’s recent talks hint at a fleeting dip right around the 2% mark, that cozy stretch is set to be a short‑lived drama. Prices are just getting back on the aggressive track, thanks in part to those pesky base‑effects that keep things from staying sweet.

Why the MPC is Still Raising Red Flags

The latest minutes from the Monetary Policy Committee (MPC) are basically saying, “Alright, let’s not get too comfortable!”

- Global tensions keep blowing up the risk‑fire.

- Corporate earnings are hovering like a high‑price balloon, adding extra hoop‑style pressure.

Labour Market: The Good, The Bad, and the Mysterious

Trackin’ jobs can feel like standing in front of a rainbow that keeps changing colour.

- Earnings cooling: The “bonus‑free” wage growth slid to its lowest in 15 months (just 6.1% year‑over‑year in January). That’s not the kind of pace that would let inflation slide back to target land.

- Despite the slowdown, real earnings still gained slightly over 2%—but it’s a bit like putting a belt around a balloon that keeps leaking.

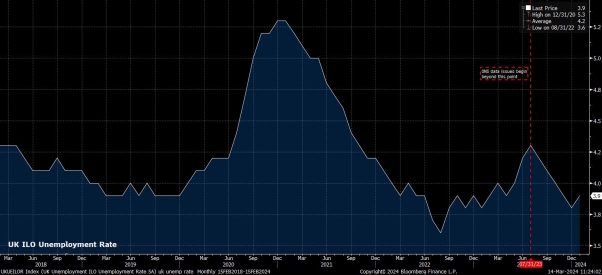

Unemployment Data: When the GPS Gets Lost

Data trouble keeps teams on a treadmill without a clear finish line.

- The revamped Labour Force Survey is slated to wrap up only by Q3—leaving the Bank of England (BoE) and other market watchers “flying blind.”

- Official numbers announced an uptick of 0.1 percentage points, bumping unemployment to 3.9% in January.

- However, the same stats hinted that out of a technical recession, the unemployment rate dropped by 0.5 points in the last two quarters of last year.

- Bottom line: read those figures with a “healthy pinch of salt.”

So, keep your eyes peeled: the inflation target might shine bright for a second, but will likely “re‑accelerate” as the second half of the year rolls in. Labour’s labyrinthine dynamics and shaky unemployment data keep everything from being a smooth ride. Stay in the loop, folks—this roller‑coaster isn’t over yet!

UK Wirtschaft: The Recession Myth Dies (And It’s Gaining Momentum)

Believe it or not, the buzz saying the recession is still looming has already lost its grip on reality. After sliding into negative GDP for two straight quarters in late 2023, the UK economy has kicked off 2024 on a high‑energy roll‑out.

January’s GDP: A Small Yet Significant Boost

- Monthly GDP growth in January – +0.2%

- This figure is a bright spark after a blurry two‑quarter downturn.

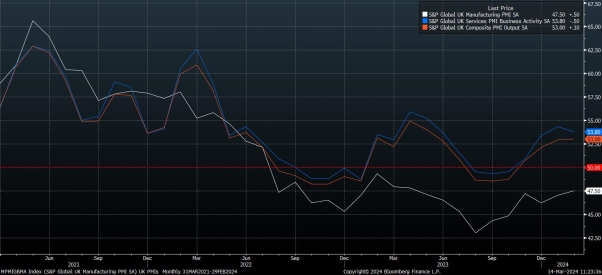

Leading Indicators: The Crystal Ball Looks Sunny

- The Services PMI hovered close to a seven‑month high last month.

- Manufacturing activities are showing signs of having hit the bottom and are slowly inching upward.

Bottom line? The economic stage is getting set for a comeback: the signals are pointing to a robust rebound, and the UK is looking every bit ready to sprint ahead.

BoE Policy Update: The Great Inflation Waiting Game

What’s brewing in the corridor?

While the economic forecast is warming a touch, the Bank of England’s inflation alarm is still ringing loudly. The MPC feels the pressure and keeps its fingers on the data pulse, waiting for a clearer signal that prices are finally easing back towards their 2 % target.

Why the “wait‑and‑see” approach?

- Inflation still too high: Even a small uptick feels like a gigantic wave to the BoE.

- Data‑driven decisions: MPs are throwing in all the numbers and asking themselves if the trend is stable enough for a rate cut.

- Spring cut on the radar: History has taught us that the first cut is likely to happen somewhere around March‑April.

Will there be any shock‑tactics?

Probably not. The March meeting is mostly a placeholder—no dramatic policy change is expected and the unanimous “no” on a post‑meeting press conference means the usual “here’s the stare‑tactics” step is left out.

What does this spell for the pound?

The pound’s fate will largely hinge on the outside world, especially how the G10 foreign‑exchange market keeps believing in the “US exceptionalism” story that has been the backbone of the greenback’s rally. In short, if the U.S. mystery sauce remains tasty, the pound will likely hover around its current level, no wild swings, just steady, data‑dependent motion.

Stay in the Loop—Instant Updates Delivered!

Ready to get the freshest news and updates from this category straight to your inbox or device? It’s effortless—just hit Subscribe below and you’ll receive real‑time alerts whenever something new drops.

- Instant notifications—no more scrolling for the latest posts.

- Mobile‑friendly delivery—read them on phone, tablet, or desktop.

- Zero lag—you’re always one step ahead of the crowd.

- Community insights—access exclusive commentary and behind‑the‑scenes content.

Don’t miss out on the buzz—subscribe now and keep your eyes on the headlines!

Subscribe