Morning Market Mayhem in the US

The U.S. trading session kicked off with a classic, no‑frills risk‑aversion mood that had everyone calling for a chill vibe. It’s all about that anti‑cyclical anxiety—right out of the old‑school playbook and still very much in vogue.

Federal Reserve’s New Focus Yields a Shockwave

Yesterday, the Fed dropped a subtle but powerful hint: it’s zeroing in on the labour market. The “bleep‑bleep” of their shift screamed—and practically shouted— that the U.S. economy is creeping into the late stages of the business cycle.

- Market agents and algorithms are now tuning in like hawks to growth data and labour snaps.

- They’re giving macro numbers the nod, putting earnings on the back burner.

- In layman terms, the Fed’s focus shift has flipped the market’s attention radar.

Jobless Claims: The First Signal to Derisk

And then came the weekly jobless claims—a surprisingly high 249k, bigger than most folks expected. This first handout set the tone for a derisking frenzy.

ISO Manufacturing: The Real Game‑Changer

Just 30 minutes after the equity market opened, the U.S. ISM manufacturing report tossed a curveball. The headline index dipped to 46.8 from an anticipated 48.8, slumping deep into contraction territory. Highlights:

- Employment sub‑component slid to a chilly 43.4.

- New orders fell to 47.3.

- Prices paid climbed from the previous month, throwing a wrench in the whole scenario.

These numbers were as grim as a bad haircut, signalling a move that would stay in play through the day and throw a dark shadow over Asia’s trading evening.

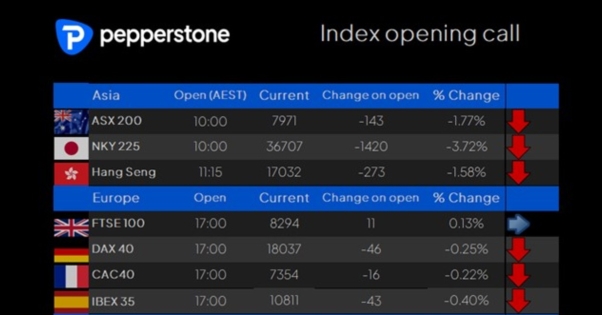

What’s Up with Pepperstone’s Index Opening Calls?

The buzz? Derisking is the first call on the table, a nod to how uneasy everyone feels. Expect the market to stay cautious, sticking to the underside of comfort while the Fed’s new focus keeps the eyes peeled for every labour market ripple.

In short, brace yourself for a lingering sense of wariness—they’ve got more data to process and a history of a stubbornly cautious market. Let’s see how the story unfolds in Asia…

U.S. Treasury Yields Drop, Market Eyes a Possible “Fed‑Fund” Party

Yesterday’s 2‑year Treasury yielded 4.28% on the way up but slid to a chill 4.13% by the end of the session, finishing flat at 4.14%—a big 11 basis point drop. Right now everyone’s watching the year‑to‑date low of 4.11% like it’s a backyard barbecue marker.

Swap Market Forecasts: Rate‑Cut Forecasts Like a Snowfall

- Swaps spit out that we’re likely to see one 50‑bp cut at the September Fed meeting, with a 25% chance.

- They’ve already priced in three 25‑bp cuts for December.

- Over the next two years, nine 25‑bp cuts are already baked into the swaps—like the market’s planning a big bake‑off.

In plain English: the market thinks the Fed is moving away from a “soft‑landing” vibe and heading toward a scenario where the fed funds rate will dip below its neutral sweet spot. Basically, the Fed might have to lower rates before it pulls back, and there might even be a “front‑loading” of cuts—now that’s a hint of chaos that can send nervous ticks flying.

S&P 500 Sector Shifts

—

Swinging Markets: Tech’s Tumble, Volatility Reigns, and Job Numbers Fear

Remember those days when US tech was the smooth ride of the session? Those good vibes are gone. The big names are getting punched so hard it feels like a bad breakup—Nvidia’s price tumble, QCOM slipping at ‑9.4%, and AMD down about ‑8.3%. Revenue headlines are still strong, but the macro mood turned sour.

Corporate credit is on a wild ride too. The HYG ETF slipped ‑0.7% and it looks like it might break those recent lows at $78. If corporate loans start looking riskier, equity will feel the heat.

Small‑cap vs. Large‑cap: Who’s Losing?

- Russell 2000 is down ‑3%.

- Large‑cap indices barely better: NAS100 down ‑2.4%.

Volatility on the Helix

Volatility—yeah, it’s the buzzword. The S&P500 burrowed 155 points wide that day. VIX is hovering at 18.5%, and traders are selling puts. Systematic momentum funds are clearing the S&P500 and NAS100 futures when they hit their triggers, while volatility‑dynamic funds quench their thirst for cash because high swings make equities feel like an ice‑melt gamble.

Late‑Stage Rally? Not So Fast

Hopefuls clinging to Amazon, Intel, Apple are getting short‑circuit. Intel took a 20% hit, Amazon slid ‑4.8%, and Apple barely nudged up in after‑hours.

Commodity Under the Microscope

Copper, the classic economic vote, sank 2.7%. Even Dalian iron‑ore futures were down. The market’s still asking: “Is this the last of the boom?”

FX Highlights

- GBP hit a new high after the BoE cut rates by 25bps—thanks to demand for USD safe haven.

- CHF and JPY found buyers—again, a sign of safe‑haven appetite.

- High‑yield, high‑beta Latin American currencies (MXN, JPY) are in freefall; carry trades are heading back to bed.

Key Focus: US Non‑Farm Payrolls

Tomorrow’s US session is going to be all about that job number. If unemployment stays above 4.2%, we’re in for a rough ride. Market players feel a sharp dislike for “bad news” for risky assets, and any slip in payrolls could pull sentiment down. If jobs hit the target, it might bring a moment of relief—but the adjustments in growth expectations mean the damage can seem bigger than it is.

For our Asian traders, you’ll want to stay on guard for any gaps when you cross over the US market—especially if the numbers hit the floors.