What to Expect from the March FOMC Meeting

Picture the Fed’s latest policy update as a quiet drizzle rather than a thunderstorm. The March meeting isn’t poised to shake things up; the big picture remains steady, and the committee’s forward‑looking guidance is likely to stay on track.

Key Takeaways

- Inflation Outlook – The latest data give officials confidence that price gains are marching back toward the 2% target.

- Rate Agenda – No big shifts in the policy stance. The fed funds rate is expected to stay firmly in the 5.25%–5.50% band.

- Market Sentiment – Money‑markets suggest a full‑stop pause for this session. You won’t hear votes for a rate swing.

Why Cuts Still on the Radar

Even though inflation is easing and employment pressures show signs of softening, the narrative of the next year isn’t all‑in‑no‑pain. Rate cuts are still on the cards—most likely starting in June—because the labor market’s cooling trend suggests room for the Fed to dial down on the Laffer curve.

In short, think of March as a calm pause: no new directions, just confidence that the ride is heading back toward the 2% target.

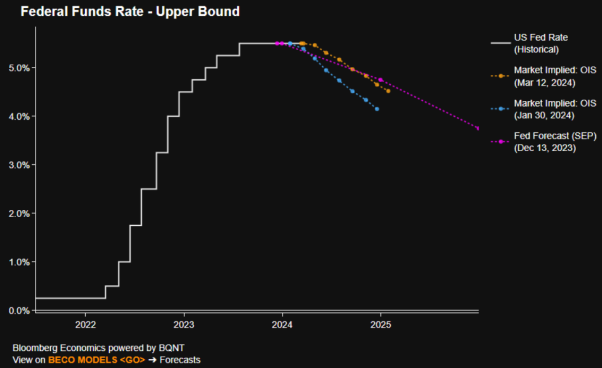

What’s the Story Behind the USD OIS Curve?

When you look at the latest USD Overnight Indexed Swap (OIS) curve, the markets are buzzing with a very clear vibe: “It’s going to be a summer of easing.” Not just from the Fed, but from almost every major G10 central bank on the block.

Key Take‑aways

- First 25bp cut in June?⏰ There’s roughly a 4‑in‑5 chance the Fed will do it. By July the move is already priced in.

- Total easing for 2024? A hefty 83bp is already baked into the curve.

- Past vs. Present? Back in January, the curve predicted a May cut and a whopping 135bp of easing by year’s end – 40% chance of six cuts.

- Recent shift? That bullish outlook has been trimmed. Now the curve sits right where the December SEP median dot would suggest, reflecting hotter-than‑expected jobs data and inflation numbers.

What does this mean for the Fed?

With the economy still humming along expectations, there’s no need for the Fed to rewrite its forward guidance. Edition: any tweak to the fed funds rate space to be data‑driven, and cuts will only roll out once there’s “greater confidence that inflation is moving sustainably toward 2%.”

Bottom line

In short, markets aren’t being daredevils—they’re playing it safe, and the Fed’s plans are staying pretty much on track, moving step‑by‑step with what the data says.

Federal Reserve’s New Economic Guidance: What It Means

Think of the Federal Open Market Committee (FOMC) as the economist gossip column. The latest update is mostly a copy‑paste from January, with the big headline: the Fed stays neutral on interest‑rate policy. There’s no sign of a big shift toward a “dovish” tone—economists just don’t see the data backing it.

Small Tweaks, Big Fluff

- Job “Moderation” Myth: Saying employment has softened since early last year feels like calling a roaring fire a smoldering ember. Even after the sharp in‑game payroll revision, headline wages have surged past 200 k for three months in a row.

- Job Growth High‑Water: The three‑month moving average is up to +265 k, the tallest since last June. The Fed would love to keep that ball rolling.

- Economic Activity: Still described as firing away at a “solid pace.” It’s all smoke and mirrors, but the traders are not flipping out.

- Inflation: It’s easing, but the Fed warns it remains elevated. Think of it as a mildly spicy curry—still a bit hot.

Summary of Economic Projections (SEP) – Classic Carve‑Up

The updated SEP is basically a carbon copy of the one released three months ago. What it tells us is that the U.S. economy is expected to do a soft landing. There’s no dramatics, just a steady ascent.

GDP and Growth Forecasts – The Real Numbers

Real GDP growth expectations from the FOMC are likely to stay close to December’s picture. The 2024 forecast might see a modest bump to 1.4% thanks to a hard‑hit services sector and hints that manufacturing output found its bottom in late 2023. In short, the economy is expected to stay resilient.

There’s nothing fireworks‑level in the Fed’s new outlook. It’s more of a polished, tongue‑in‑cheek note that “things are looking good enough.” For now, the big story is: stay neutral, keep an eye on job growth, and hope inflation stays on its down trip.

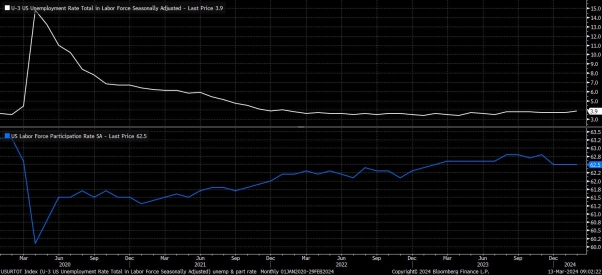

Job Market Outlook 2026: What’s the Buzz?

Even though headline unemployment jumped to a surprise 3.9 % in February, the big kahuna FOMC folks are probably still holding their breath—one month’s data isn’t enough to predict a full-blown trend. Think of it like watching a single season of a show and declaring it a masterpiece; you’ll miss the spoilers.

Why the Forecast Still Makes Sense

- Growth’s doing its best hustle: The economy keeps showing resilience, so the overall outlook for jobs remains upbeat.

- Participation isn’t at its peak: Labor-force folks are hovering about 0.3 percentage points shy of the Q4 ’23 highs—so it’s unlikely anyone will find a huge surge in job losses.

- Some job market breathing room needed: To keep the sticky services inflation from clogging the traffic, a gentle loosening of the labor market will probably come into play.

Bottom Line

All things considered, the forecast still pins unemployment at 4.1 % through the end of 2026. That number feels about right—like a perfectly brewed cup of coffee: not bitter, not too sweet, just the right balance.

Inflation Update: Will the Numbers Really Change?

Hey, folks! If you’re like most of us worried about how many penny‑cents our wallets might lose this year, you’ve probably heard chatter that inflation is creeping up. But let’s break it down in plain English—and maybe chuckle a bit while we’re at it.

What the Numbers Are Saying (And Why They’re a Bit Confusing)

- Headline and Core PCE forecasts seem pretty solid: Expect both to rise about 2.4% in 2024, easing to 2.0% by 2026. Surprisingly, those predictions are holding strong even after the recent hot CPI prints.

- Three straight hotter-than-expected CPI numbers have rattled investors. But it’s more about the “recipe” of the CPI basket than a genuine rise in everyday prices.

- The key ingredient? Shelter. In CPI, the “Owners’ Equivalent Rent” (OER) line line up with roughly a third of the core CPI figure.

- OER’s recent skew stems from BLS’s re‑weighting tweaks—everything from grocery baskets to ghost‑like pricing ghosts—leading to inflated surprises in CPI.

- Contrast that with PCE. It’s a leaner eatery and OER makes up only about a sixth of its basket. So the influence of that “shelter wobble” is far less pronounced.

Why the Fed’s Green‑Light PCE Looks Safer

- PCE places socks (shelter) at the bottom of the priority list. That’s why it’s likelier to stay on course even though CPI’s mouth is on fire.

- Because PCE’s sensitivity to shelter shocks is reduced, the forecast of 2.4% inflation in 2024 stays on track.

- Even if those CPI prints look like a small storm, the Fed considers the actual impact on the economy a bit more understated.

Bottom Line

So what’s your takeaway? The pandemic‑messed CPI prints are mostly a mirror effect of how shelter prices were handled. The PCE, with fewer “shelter shenanigans,” is likely to keep inflation forecasts steady. That means, for now, the chances of a major headline change remain pretty low.

Stay tuned, keep an eye on the numbers, and if your budget feels like it’s doing a salsa dance, remember: the core picture is looking clear enough to keep the dance floor.

— Your friendly inflation analyst (and occasional comedian)

What the FOMC’s “Dot Plot” Is Likely to Be Now

Picture the Federal Open Market Committee’s famous “dot plot” as a scatter‑graphed version of a dice roll. The dots show where each member thinks the U.S. interest rate should sit in future years. With the economy humming along on just about the same level it has been for months, the plot is probably not going to make a dramatic exit.

Fast Track 2024: The Mid‑Century (4.625%) Target

- Most participants still expect the fed‑funds rate to settle around 4.625% in 2024.

- That tier means the board is eyeing roughly 75 basis points of cuts over the year—a modest, but steady easing.

2025 & 2026: A Slide Toward Readiness

- By next year, the target drops to 3.625%, and then further to 2.875% in 2026.

- Below that, the “long‑run” figure hangs at 2.5%, effectively a baseline the committee uses as a safety net.

So What About the Spread?

The wide 2024 expectations range from 3.875% to 5.375% tells us a lot about the atmosphere in Washington. If the spread shrinks in the next plot, that’s a subtle nod that policymakers feel more confident about the economic outlook. A tighter spread is like the committee saying, “Everything’s looking good—let’s bite our nails and make the final decision.”

Bottom Line

In short, the big picture remains stable. The dot plot will probably stay similar to December’s, but mark your calendar for a slight narrowing of the dots. That could mean both a smoother path to policy tightening and a more united front among the FOMC members—nice, isn’t it?

Feds, Rates, & The Long‑Term Gamble

Even if the Federal Reserve‑dot‑plot starts looking a little cooler than usual, the game of inflation control remains a high‑stakes circus. Two key policy players—currently the median expectation holders—could, with a single 25‑basis‑point bump, shift the median outlook. That’s the math (and the risk). Yet, no Fed chatter so far has teased this shift. Still, the jobs market is tight and inflation has been curving like a roller‑coaster; nobody can confidently ditch the possibility.

Long‑Run Rates Are Turning Heads

- Expectation shift warning: The Cleveland Fed’s Mester, a member who’s on the brink of retirement, hinted she’s thinking about a higher long‑term target. It hasn’t yet taken hold among the FOMC, but the mood is changing.

- Market reaction: If the Fed tweaks its long‑term rate upward, markets could reprice a faster, gentler easing cycle to bring policy back to “neutral.” Think of it as a mid‑term wind‑up against risk assets and Treasuries.

QT Tapering: Curtain Call in May?

While the March meeting will headline dot‑plot updates, it also flips the switch to deeper talks about tapering the ongoing quantitative tightening (QT). A formal decision on when QT will wind down feels like a splash of water—“come at the May meeting, but the real heat is in June.” Why? Overnight reverse repo usage slows, and the flow of bank reserves is creeping toward the “lowest comfortable level of reserves” (LCLoR). The outcome? Less aggressive reserve removal and a steadier path for monetary policy.

Bottom line: keep an eye on the dot‑plot. The Fed’s stance can pivot with small tweaks, and those changes ripple across markets. A higher long‑term expectation signals a less aggressive easing future, while the QT taper timeline nudges the financial system toward a calmer rhythm. Stay tuned, and be ready for the next wave of surprises.

Powell’s Post‑Press Conference: Expect Nothing but the Same Old Song and Dance

After his “big‑eye‑in‑the‑sky” sitting on Capitol Hill early March, Chairman Jerome Powell is set to meet with the media for the usual round‑trip disclosure—an almost perfect repetition of what he said to the congressional panel two weeks earlier.

What’s on the Menu?

- “It’s probably a good idea to cut rates this year” – the same sweet spot he’s occupied for the last few hours.

- The FOMC will “carefully remove” their restrictive policy—no dramatic plot twists here.

- Big brother plans on keeping the inflation gears running, waiting for that green “2 % target” to start the countdown.

So, in plain English: the Fed will keep nudging rates downward, but only when it feels the track of prices is truly sliding back to the 2 % mark.

What Does That Mean for Wall Street?

The market’s got all the space to breathe and grow. Equities will rise because of the “least resistance” path—no laborious policy shifts or surprising rhetoric are on the docket.

And the Dollar?

With a steadfast policy stance, the greenback is expected to continue its climb.

Bottom line: expect a dose of repeated rhetoric and no dramatic surprises. The Fed’s still playing the same tune.

Possible Market Moves After the March Decision

Picture the Fed’s dot‑plot as a wobbly rug. If the median for 2024 turns out to be a modest 50 bp instead of the expected 75 bp, the rug will shift just enough to send a ripple through the markets. The result? A flier “hawk‑flight” that could drag equities and Treasuries down while giving the greenback a little lift.

Why the Hawkish Hazard is Real

- Discounted Cuts: A 50‑bp number looks like a shortcut that keeps the Fed’s tightening tone in the spotlight.

- Asset Flipper Effect: Stocks and bonds might feel the squeeze as investors anticipate higher rates, while the dollar could see a cheer‑up from the upside of stronger policy.

- March Momentum: The March decision already nudged markets toward a hawkish stance, and there’s little fresh data pushing for a more dovish pivot.

What the Data Says (and Doesn’t)

At present, there’s essentially no evidence to justify a more dovish tilt. The markets have already priced in an outlook based on the current median dots, so any shift toward complacency would have to come from new, compelling information.

Takeaway for the Everyday Investor

- Keep your eyes on the dot‑plot updates—they’re the Fed’s mood swings.

- Expect a potential dip in equities and Treasuries if the cuts count is narrowed.

- Don’t forget the dollar may climb when rates tighten.

Bottom line: stay ready—whether the Fed plays a hawk or a dove, the market will dance to its rhythm.