Intel: From Tech Titan to Comeback Kid

Once the powerhouse of PCs and servers, Intel’s mighty reign has been challenged by delays, fierce rivals, and a rapidly changing tech landscape. Under the fresh haircut of CEO Pat Gelsinger, the company has kicked off a bold makeover, aiming to regain its sharp edge and venture into new territories. The current share price has crept back to its 2012 lows, and the market valuaton hovers near the bottom‑line liquidation figure—making Intel an intriguing, if risky, pick for savvy long‑term investors.

What Drives the Current Race?

- The IDM 2.0 Playbook: A revamped, in‑house design‑manufacturing strategy that promises better control.

- 18A Tech Process: The next generation of chips expected to cement Intel’s place at the forefront of semiconductor make‑up.

- Big Cuts: The firm is trimming nearly 15,000 jobs to lean and stay profitable.

But the road is anything but smooth. If Intel fails to hit profitability or send clear signals soon, its fortunes could look bleak—think of a namesake as iconic as Nokia or Kodak, spectacularly outpaced by nimble competitors in a reshaped tech map.

Is Intel a Bargain or a Value Trap?

On one side, the price looks “cheap” and the story of a comeback can inspire. On the other, some fear that the challenges are too massive—and that even a courageous downsizing spree might be insufficient. The key question: Will Intel’s revival attempt actually lift it off the ground?

What’s Next for the Giant?

Intel is hunting for a future that feels both hopeful and realistic. Whether it’s a strategic underdog or a sweet deal for diligent investors, only time—and a few well‑executed steps—will tell.

From dominance to problematic transformation

Intel’s Big Shift in the Chip World

Founded in 1968, Intel carved out a legacy as the king of semiconductors—especially in the processor arena. But a mix of delay in new manufacturing tech, fierce rivals like AMD and Nvidia, and the meteoric rise of artificial intelligence has thrown the company into a rough patch.

Why the Slide?

- Tech hiccups—Intel was slow to roll out advanced production lines.

- Intense competition—both AMD and Nvidia keep pushing Intel’s limits.

- AI surge—the market’s shift to AI‑focused chips caught Intel off guard.

- Tariff misstep—missed opportunities linked to trade duties on foreign goods.

Stocks Take a Nosedive

The fallout has driven Intel’s share price back down to levels seen in 2012, rattling investor confidence on the company’s future. While the dip feels like a setback, there’s a silver lining for those who are looking for a long‑term play.

Pat Gelsinger’s Mission

Pat Gelsinger returned to the helm in 2021 with a bold plan: revive Intel’s former glory. His strategy involves two main moves:

- Reclaim leadership in legacy products—solidify the CPU lineup that has powered the world for decades.

- Expand into new frontiers—dive headfirst into AI chips and data‑center solutions that shape tomorrow’s tech.

So, while the road ahead looks tough, Intel’s new direction under Gelsinger might just turn the tide—and turn that low price into an attractive long‑term opportunity.

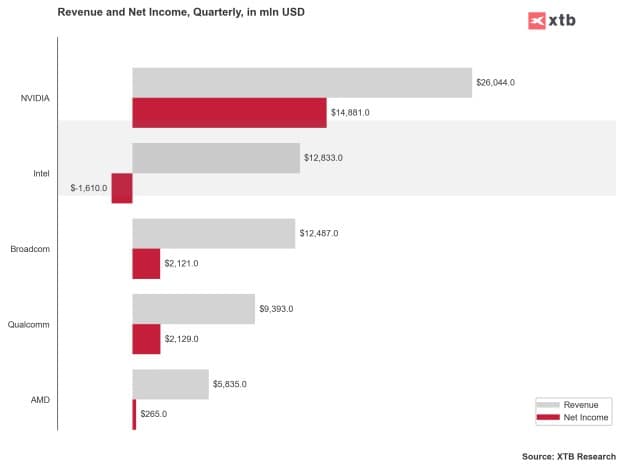

Intel’s Five-Year Drought: How the Goliath’s Growth Stalled

There’s a rough patch in the semiconductor jungle: Intel, once the king of chip makers, is showing a tired, tired face when you compare it against its rivals. If you’ve been following the market this past year, you’ll notice the title of the story everyone’s reading is a bit grim: Intel looks pale, fresh water lacking after five years of long, hot summer.

What’s up with the numbers?

- Sales slump: In absolute terms, Intel’s revenue dipped about 10% year‑over‑year in 2023, yet competitors like AMD and Nvidia lifted off.

- Gross margin: While the Giants’ margins improved after a fresh supply‑chain tweak, Intel’s stayed stuck right around the 35‑40% range, leaving a big gap.

- R&D spend: Intel poured roughly $10B into research, but that still feels like a penny‑pocket in comparison to the “money‑miser” style of AMD.

Why the trend looks scary now

Think of it like a marathon: the starters were all going at pack speed, but Intel is lacing up and taking a nap right before the second mile. Over the last five years, it failed to capture the valley of AI processors, a decisive sweet spot for modern data centers.

The market’s reaction

Investors have been swinging for a 5% slide in Intel’s share price, while its tech‑smarts rivals keep the momentum. It’s almost like someone in the pit crew was watching the tape from the other team and discovered a hidden shortcut.

So what’s the takeaway?

Tread carefully, tech fans. Maybe it’s not a total collapse—Intel’s still a rock in the silicon space. But compared to its rivals, the new generation of processors feels rather “meh.” And the five‑year window screams that more than just a one‑off issue.

Source: Bloomberg Finance LP, XTB

Will revenue diversification help it survive?

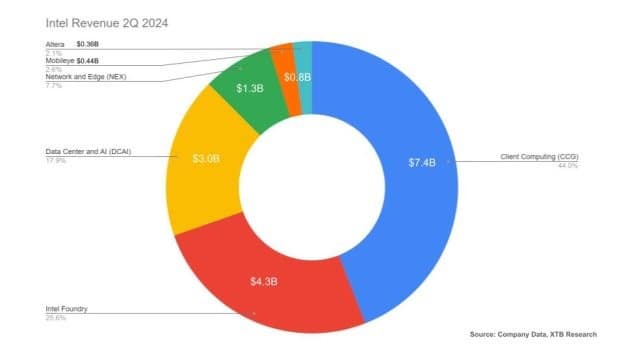

Intel: The Big Tech Powerhouse

Ever wonder where the chips behind every gadget you love come from? Meet Intel – a company whose name feels like the last word in your high‑tech wish list. Here’s how the tech giant splits its mojo across three major arenas.

1⃣ Personal Computers & Mobile Devices (CCG)

- Biggest slice of the pie – over half of Intel’s revenue flows from PCs and mobile gadgets.

- From the humble wall‑mounted motherboard to the sleek laptop that powers your Zoom meetings.

- Think of it as the “bread and butter” that keeps the rest of Intel’s projects humming.

2⃣ Data Centers & Artificial Intelligence (DCAI)

- Second in size; the playground for cloud computing and cutting‑edge analytics.

- These server processors are the brains behind everything from web services to advanced machine‑learning models.

- Essential for anyone who wants to crunch numbers faster than a caffeinated squirrel.

3⃣ Networks & Edge Devices (NEX)

- Where 5G and the “Internet of Things” meet – a bonafide growth hotspot.

- Edge computing means data gets processed right where it’s generated, slashing latency.

- Imagine your fridge or your car talking to each other faster than a gossip outlet.

Other Ventures

In addition to the core segments, Intel is juggling:

- Autonomous Driving – thanks to Mobileye, your car’s autopilot is getting smarter.

- Low‑Power Systems – the 3rd‑party IFS chip building keeps devices tiny but mighty.

- Programmable Logic – think of FPGA chips that can be re‑wired on the fly.

So next time you tap your phone or open a spreadsheet, remember that Intel’s masterminds have probably been working behind the scenes to make that experience buttery smooth. It’s not just a chip company; it’s the backbone of the digital world!

Intel’s Margin Crunch: What’s Up?

Intel’s profit margins are taking a hit. Gross margin has slid from the 55‑60% sweet spot it once enjoyed down to the roughly 38‑40% range these last few quarters.

Why the Drop?

- Heavy R&D Spend: The company is pouring cash into next‑gen tech that isn’t turning back the money quickly.

- Staying in the Game: Competition is fierce, so Intel keeps pushing the envelope—costs stay high.

- Low Plant Utilization: Factories aren’t running at full capacity, leading to wasted efficiency.

- Market Slump: The PC and server boom after the pandemic has cooled off, so demand is shrinking.

Financial Pain Points

With these challenges mounting, Intel is taking a tough route: a planned 15% reduction in workforce is on the cards, signaling a rough patch in its financial future.

Source: XTB Research

Why is Intel valued near liquidation value?

Intel’s Valuation Puzzle: Why the Big Chip Maker Is Trading Low

What’s the “real” value of Intel?

When we strip out the intangible fluff, Intel’s tangible book value per share sits at about $19.51. That means the company owns solid assets—like its chip factories in the US, Israel, and Ireland that together hash out to roughly $80 billion—minus all the intangible baggage.

Memo: Cash, Patents, & Batteries

- Cash & quick assets: Nearly $29 billion sits in cash and short‑term investments as of Q2 2024.

- Patents & know‑how: Thousands of semiconductor patents and in‑house design expertise.

- Strategic bets: A stake in Mobileye, the Israeli autonomous‑driving tech firm, plus a handful of promising start‑ups.

Why the Market’s “Low” on Intel

Intuitive? Not really. The chip titan has slipped out of profitability, is draining cash, and even stopped its long‑running dividend payout. Meanwhile, the race to catch up with lightning‑fast rivals like NVIDIA, AMD, and Broadcom demands hefty spend—think newer processes and AI‑specific silicon.

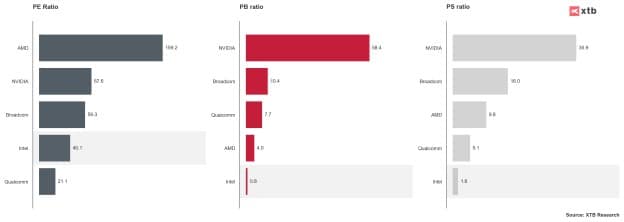

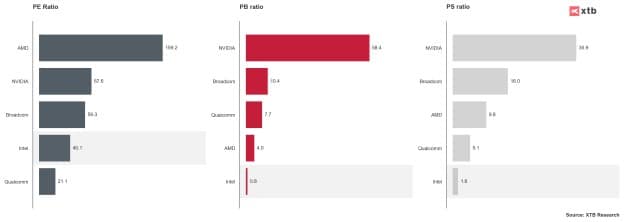

Price Ratios: The “Bull Market” Blip

Let’s look at the numbers.

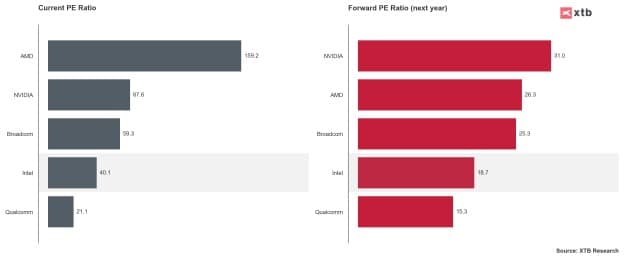

- Price‑to‑Earnings (P/E): Intel’s P/E is currently the lowest on the tech block; a consequence of its profit slide.

- Price‑to‑Book (P/B): A hungry 0.8—indicating investors view the company as under‑priced for its tangible assets. For comparison, NVIDIA’s P/B sits at a staggering 58.4.

- Price‑to‑Sales (P/S): Intel’s 1.6 is dwarfed by NVIDIA’s 35.9.

Bottom line: The market thinks Intel is a sinking ship on paper, but if you dig deeper you’ll find robust facilities and a treasure trove of patents. Whether that can propel the company back to the giants of the industry remains to be seen.

Intel’s Rocky Ride: Why the Numbers Don’t Lie

Bottom line: Intel’s current valuation feels like a quiet shrug from the market—investors just don’t see the future sparkle they’re hoping for.

- Investors are gushing about NVIDIA and AMD, betting big on AI and cutting‑edge computing. Those companies fly high on optimism.

- Intel, on the other hand, is stuck in a more cautious lane. The low valuation ratios hint at doubts: “Can Intel pivot, win back the tech crown, and keep up with the next‑gen chip players?”

- Analyst predictions for the coming year? They keep the forward P/E hovering around 18.7—pretty low compared to its rivals.

Think of it this way: Intel’s like that friend who’s always saying “I’ll get it right next time.” The crowd’s still waiting for the makeover to happen—until then, the confidence scale stays at a frustratingly low mark.

Is Intel in danger of being removed from the Dow Jones and other major indices?

Intel’s Shrinking Footprint in the Big Three Wall Street Indices

When you hear “big names” in the stock market, you expect giants. But Intel’s share in the major indices has been sliding like a slippery chip. That decline isn’t just a quiet dip in the numbers—it ripples through ETF strategies and could alter how the market sees Intel.

Drop in the S&P 500

In the S&P 500, the most‑watched index on Wall Street, Intel’s weight is now only 0.19%, a hit from more than 1% a few years back. That’s a substantial shrinkage, especially when you compare it to the heavyweights that sit at 1% or higher.

Shiver in the NASDAQ‑100

The tech‑centric NASDAQ‑100 models Intel’s influence as just 0.59%. In a list of high‑growth companies, that number is barely noticeable.

Near‑Zero in the Dow Jones Industrial Average

Perhaps the most concerning is Intel’s placement in the Dow. With an odd 0.334%, it’s last on the list of 30. That low score raises the risk that Intel could be dropped when the index is next re‑balanced.

- S&P 500: 0.19% – a big drop from >1%.

- NASDAQ‑100: 0.59% – barely a footnote.

- Dow Jones: 0.334% – the last spot, no guarantee it stays.

For ETF managers, these changes mean recalculating holdings to keep the hedge ratio tight. Intel’s retreat may force shifting funds away, impacting the broader semiconductor outlook.

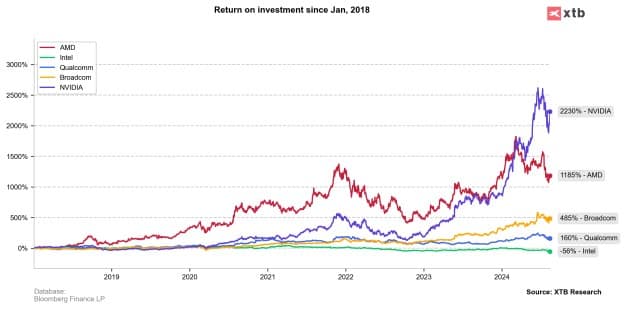

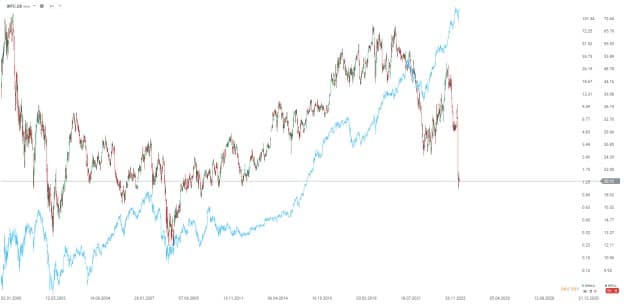

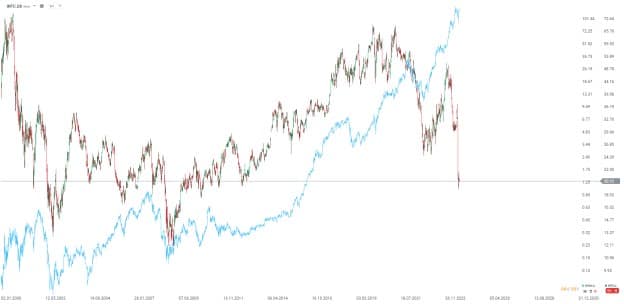

On the chart, Intel is back to 2012

When you look at this graph through a crystal ball, it’s like spotting your high‑school photo: things just went back to 2012. But remember, three years ago the company was worth three times as much—talk about a rollercoaster ride!

Nvidia: The Quantum Leap

Local Lows: $13 Revisited

Prospects of a Comeback

I’m ready to rewrite your article, but I need the text you’d like me to transform. Could you paste the content (without any HTML tags) so I can get started?

I’m ready to rewrite your article, but I need the text you’d like me to transform. Could you paste the content (without any HTML tags) so I can get started?

An uncertain future with a tight schedule

Intel’s Bold Leap Back Into The Chip Arena

Intel stands at a tipping point: it’s setting its sights on reclaiming the throne in semiconductor manufacturing with the IDM 2.0 playbook that made the headlines back in 2021. The strategy rides three top‑gear pillars – crank up capacity, outsource strategically, and become a world‑class fab.

New‑Gen Process Roadmap (and a dash of ambition)

- 2024 – Go live with Intel 4 (7 nm) for a shake‑up of internal product lines.

- 2025 – Drop Intel 3 and Intel 20A (2 nm) into the production line.

- Beyond 2025 – Fast‑track the groundbreaking Intel 18A (aiming for around 1.8 nm).

The company has already started rolling out volume production on the Intel 3 node, gifting both its own gear and third‑party clients a potent boost: a new FinFET design and a high‑density layout that’s a serious threat to the TSMC‑centric market.

Foundry Services Take the Stage

Intel’s Intel Foundry Services (IFS) is opening its doors to external customers. A shining example? A $15 billion partnership with Microsoft to churn out custom chips. The headway on 18A positions Intel to stand toe‑to‑toe with TSMC’s N3, giving end users a fresh alternative to the usual TSMC route.

Why It Matters

TSMC currently rings the bell for advanced manufacturing and is betting that by 2028, AI processors will bring in more than 20% of its revenue – growing at a dizzying 50% year‑over‑year. Intel can’t afford to lag; the AI surge is reshaping the industry faster than we can say “chip revolution.” Plus, the continued dependency on TSMC’s tech puts Intel at risk if geopolitical tides shift.

Building the Future – Literally

- Expand existing fabs and erect six fresh plants across Arizona, Ohio, and Germany.

- Leverage hefty government subsidies and customer commitments to drive the capital rollout.

- Invest huge amounts in cutting‑edge tools: EUV lithography, RibbonFET (GAAFET), and PowerVia (backside power delivery).

Winning the Game

To outclass TSMC, Intel needs to deliver on its technology promises and attract a steady stream of clients to IFS with competitive pricing and stellar build quality. The belief that it can juggle external production without skimping on its own high‑performance chips is the secret sauce.

In 2025, most output will still lean on the older 7 nm and 10 nm processes, which may cap the margin upside from fresh EUV launches. Still, Intel is pouring in more than double the R&D dollars of Qualcomm, keeping the innovation pipeline humming.

The Path Ahead

Intel’s ambition: to go beyond fabs & drop in full system solutions, aligning with the massive computational demand unleashed by generative AI.

Success hinges on rolling out this tech schedule on time, signing up the right customers for IFS, and wrangling costs. If it all clicks, Intel could very well become the new contract‑manufacturing contender next to, and in some markets ahead of, TSMC.

Summary

Intel’s Big Gamble

The New Playbook – IDM 2.0

Intel has rolled out a fresh strategy called IMD 2.0, aiming to smash old limits:

• New process tech – the next‑gen chips that could outpace every rival.

• Foundry services – monetizing wafer capacity for the masses (think “chip‑share”).

• AI & high‑speed computing – tapping into the sectors that are exploding faster than a crypto‑boom.

Why the Price Looks ‘Bargain‑Bear’

Intel’s shares are dip‑priced versus its peer group, giving a potentially big upside if the next step works. Imagine the market moving from “where did that go?” to “got that right!”.

What’s the Magic KPI?

Two things will be a game‑changer:

- Achieving 18‑A chip competitiveness – the sweet spot for modern processors.

- Improving operational efficiency – turning pennies into dollars like a well‑trained accountant.

If those happen, Intel could not only reclaim its lost territory but also become a heavyweight in the AI boom.

Risk, Patience & Potential Returns

Short‑term noise? Absolutely. Long‑term horizon? Big.

Breach the finish line, and the stock could skyrocket – a nice payoff for those who roll the dice.

Stay in the Loop

Want real‑time updates on this story? Subscribe now and get the newest info straight to your device.