Fed’s Roadmap Straightened After April CPI

Right after the April CPI release, the market has finally sorted out where the Federal Reserve should be headed. With the June FOMC just under a month away, everything feels like it “should” be doing exactly that.

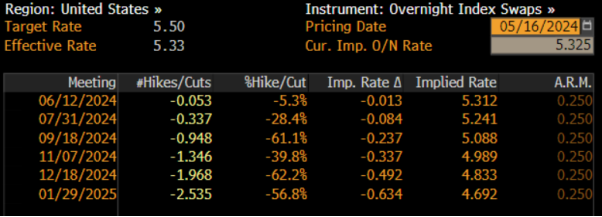

USD OIS Curve: The Coffee Breaks Are Coming

- 50 basis‑point cuts this year are dressed up in the curve – basically the market is betting on two short‑term “coffee breaks.” One in September, the other in December.

- At each of those two meetings, the odds are about 95% that the Fed will swing its rate‑theater tongue.

- Effectively, the market’s already calcified on the outcome – it’s as if the big shot, the Fed, was just sending the memos.

So, the short story: after April’s CPI glow-up, the market’s playing it safe, and the odds for rate cuts by September and December are practically a done deal.

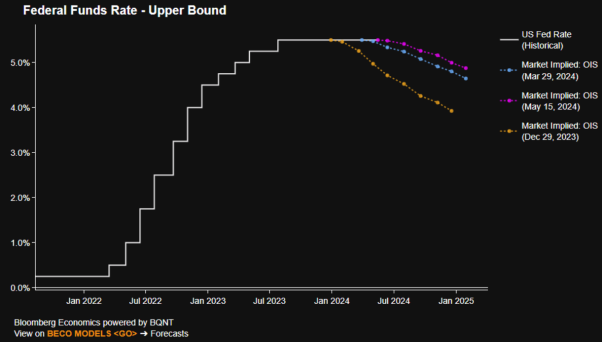

Fed Rate Outlook: A Wild Ride With a Dash of Swagger

Picture this: the market’s been juggling a hawk‑like outlook, dreaming of six 25‑bp cuts to the tune of 2024 money markets. By the end of Q1, that anticipation turned into an 85‑bp easing ghost‑town – kinda like a candle-quiz in a dark room.

- Hawk‑ish vibes – The market’s still perched higher than it was mid‑first quarter, as money markets sprinkled in up to six 25‑bp cuts.

- Risk? Not a big deal – The real buzz isn’t about that lingering 85‑bp goose‑flying figure; it’s about the Fed’s confidence runway.

- The Fed’s playbook – They have the muscles (willpower and policy tools) to flip the switch to a cut on the next move. Yes, the Fed funds rate is heading toward a downward glide.

- Inflation’s chill approach – April’s core CPI slid to a near‑3‑year low of 3.6% YoY. That’s like a cool breeze telling the Fed to hit play on the rate‑cut switch.

Bottom line? We’ve got a Federal Reserve that’s ready to lace up its shoes, arrow‑down on the rates, and show us just how slick cut maneuvers can feel.

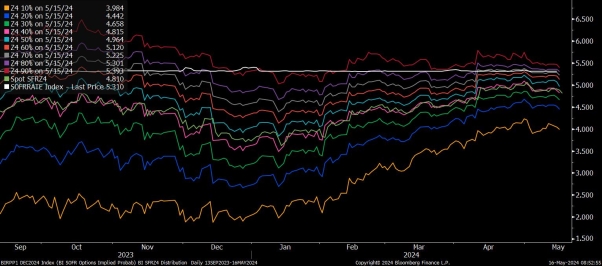

SOFR Options Reveal the Real View on Fed Rates

When you glance at SOFR‑based options, you get a pretty clear picture: folks in the derivatives world are basically saying there’s only a 3% chance the Fed will hike again before the year ends. And that tiny probability? It’s not about betting on policymakers; it’s more about hedging flows—safeguarding against that unexpected bump up.

What’s Driving the Low Odds?

- Chair Powell’s Take: In May’s FOMC press briefing, Powell made it crystal clear that a rate hike is “unlikely” to be the next move.

- Inflation Looks Cozy: Recent data is showing inflation at more promising levels—nothing crazy like the old days.

- Economic Indicators Stalling: Cooler April retail sales and Q1 GDP growth slipping to under 2% annualized QoQ give a hint that the economy’s pace might slow, not speed up.

- The Hype Dies: All of these factors have combined to make the idea of another hike feel as dead as a stone—killing that rumor behind the scenes.

Bottom Line

In short, the market’s green‑light green‑light: there’s almost zero real appetite to chase a new rate hike. Derivatives are playing it safe, hedging against the faintest buzz of policy tightening, while the real economy’s signals justify keeping the chance to a barebones invite—just a shoebox of probability.

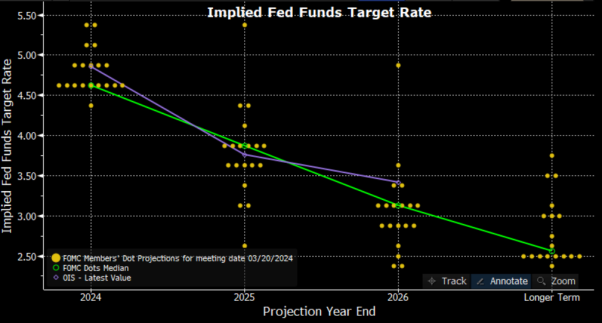

Fed Talk: How Much to Cut the Fed Funds Rate?

In March, the Federal Reserve blew out the latest dot plot—basically a scatter chart showing where the fed funds rate might land by the year’s close. The median line pointed to a range of 4.50% – 4.75%, which translates into about 75 basis points (bp) of cuts for this year.

But don’t hit the brakes just yet. That pace of easing is still on the table—especially if the labor market suddenly takes a nosedive. Still, once the July “SEPs” (the Fed’s quarterly economic snapshots) hit the stage, we’re likely to see a sharper, more hawkish line.

Here’s the most probable play:

- Only 50bp of cuts are projected for the year’s end.

- Fed chatter suggests we’ll need to give the policy a little more breathing room: delay the first cut and trim the total amount of easing so we don’t have to slash aggressively.

- If even one committee member bumps their 4.625% end‑24 estimate up to 4.650%, the median dot could jump by 25bp.

Bottom line: the Fed’s future path is like a game of economic hopscotch—one step at a time, watching for any sudden twists in the job market.

Fed’s Dot Plot Looks Set to Align with Market Sentiment… and Says, “Here We Go”

When the Federal Reserve’s dot plot gets a makeover, it’s not just a cosmetic change—it signals that the Fed and the market are finally on the same page. That’s a pretty rare moment in an otherwise foggy year.

What’s on the Horizon for Rates?

- Front‑end neutral stance. The short end of the curve is looking calm. Think of it as a “hold your breath, no big changes” vibe.

- Long‑end volatility continues. The market keeps nudging the long end down because investors are still digesting that the Fed’s target is an inflation band with 2% as the floor, not a hard 2% ceiling. That subtle nuance keeps the tail of the curve a bit restless.

- Neutral rate climbing. As the neutral rate ticks higher, expectations shift, but the overall tone stays balanced.

What About the FX & FI Market?

Expect a smoother ride for the short‑term. With no major macro events on the calendar until the April PCE report next Friday—and that report is fairly predictable once you’ve seen the PPI and CPI numbers—volatility should ease.

Next, the May jobs report on June 7th might stir the pot a bit, but it won’t be a major shockwave. Investors are cooling off, giving markets room to breathe.

Dollar’s Medium‑Term Dance

Keeping it simple: the greenback is likely to stay in a range of 104–106.50 over the coming months. That’s the sweet spot where the dollar neither swoops too high nor plummets too low—just a steady stroll.

Why It Matters

- Fed and market alignment reduces uncertainty.

- Calmer FX & FI markets mean fewer surprises for traders.

- Dollar’s predictable band helps businesses plan ahead.

So, as the dot plot refines itself, the Fed and the market seem to be in sync—an unlikely duet in a year full of detours. Keep your chin up; the ride ahead looks smoother.