Calming the Commotion: A Brief Market Check‑In

Fewer thrills and more chill

It’s a quieter week in the money world – the kind that makes you feel like you’re watching a slow‑moving river. This low‑noise backdrop is the perfect chance to recap the last few weeks of policy mumbo‑jumbo.

The “tend-overs” we’ve seen

- Central banks in developed markets keep saying “hang tight” – but they’re in fact leaning toward easing.

- Risk assets have a little extra wind to ride on, thanks to this calm, supportive environment.

- Inflation is inching back close to that 2 % target – a fact that has turned the Fed’s fingers a bit more rumpled.

What’s slipped through the cracks?

Nothing radical has been added to the plot. Instead, the latest statements reaffirm the same themes we’ve already been guessing:

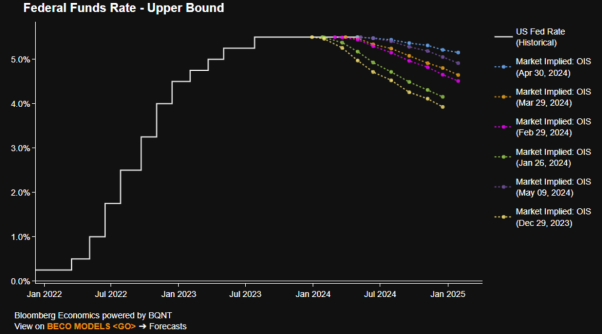

- The Fed is apparently keen to kick off an easing parade, either because it trusts inflation will keep falling,

or because a shock to the job market dampened the sluggish confidence the “bounce” was supposed to bring. - The jobless‑claims surprise, rattling Europe, is being quietly watched by the bankers who could slam the discount door in July or August, if the data trembles faster than expected.

ECB’s early exit strategy

The European Central Bank has already set the stage in March: cut the deposit rate in June, and keep the ball rolling on a June rate drop if the April CPI data show the 2 % north‑pole target has been reached.

Swiss and Swedish vibes

Switzerland’s SNB slashed rates by 25 bp in March and is likely to do the same again next month. The Riksbank in Sweden is also stepping sideways, trimming by 25 bp this week.

Bank of England gets the green light, but with a cautionary twist

After a dovish blurb and a press conference, a Deputy Governor’s surprise dissent kept the cut door in June wide open – waiting for the data wave to roll in.

Markets aren’t all about the rates

Let’s not forget the balance sheet shuffle. The Fed is trimming the speed of its quantitative tightening (QT), shrinking the cap on Treasury run‑off to $25 bn a month. The Bank of England could wrap its gilt sales at the September review if repo demand shows a tidy uptick.

What this means for the next waves

- We’re looking at a mix of banks easing, ramping up to ease, and holding off for spare bull power.

- Liquidity conditions are likely to keep swelling toward the year‑end, supporting risk‑bearing assets.

- The real question isn’t “how many cuts will the Fed take?” – it’s that if the policy team can cut, they will. And they’re doing it as the year advances.

Bottom line

In plain English: the market’s breathing easier. Central banks are taking the long‑term lull in boom‑bust to coach the economy. Keep an eye on growth numbers, and you’ll know when the next round of cuts rolls in. For now, a calm week truly means a calmer week for markets.

Market Pulse: Why Risk Assets Keep Climbing

Point‑blank Forecast

Unless the Fed suddenly flips into full‑on hawkish mode—which feels more like a rumor than a reality—the next trend for risk‑takers is simple: keep moving higher over the short and medium term. The current policy “put” is hanging out like a shoulder‑covered security blanket, letting everyone know the policymakers have their backs again. That assurance just fuels confidence to jack up the risk curve.

Old School Wisdom

- “Don’t fight the Fed.” – Everyone should remember that lesson, especially the long‑term equity bears who keep losing sleep over market swings.

- When central banks tighten up, markets are on a new roller‑coaster that a few people snag onto and enjoy.

- Trying to counteract the Fed’s easy‑going stance is like bringing a blizzard to a sunny beach—just don’t.

Stay in the Loop

Want the real‑time scoop? Subscribe now and get the latest updates straight to your device—no more scrambling for market news in the morning. Keep yours ready for the next move!