Stocks Reach New Highs as Treasuries Surge and the Dollar Slides

Wrapping Up a Quiet Friday

Friday landed on a relatively calm note—data and news were scarce, and market activity was thinner than usual as U.S. investors turned in for a long weekend of Thanksgiving festivities.

Eurozone Inflation: A Glimmer of Insight

- Headline CPI climbed 2.3% YoY last month, right on target.

- Core prices ticked up 2.7% YoY, unchanged from the prior month and just a touch softer than analysts had pegged.

While the numbers paint a pretty ordinary picture, they’re unlikely to shake the European Central Bank’s strategy. A 25‑basis‑point cut is still the most likely move for the next fortnight, though every now and then, the market whispers a 50‑basis‑point “surprise.”

That surprising swing doesn’t feel very realistic right now—no ECB speaker’s calendar has hinted at a big jump. The real debate will soon move to whether the deposit rate should dip below the neutral point (roughly 2%) in mid‑next year.

Implications for the Euro

A fully “loose” stance could have a dampening effect on the euro, especially as other central banks stick to a neutral stance and take a “wait‑and‑see” approach. While the euro struggled to break even $1.06 at the end of last week, it was wiped out on the back‑end, and enthusiasm seemed to be hitting a plateau.

U.S. Dollar: A Bit of Trouble

The dollar trailed the rest of the week, easing particularly against the Japanese yen. The USD/JPY slid back beneath the 150 mark for the first time since mid‑October after Tokyo’s stronger‑than‑expected CPI figures pushed expectations that the Bank of Japan will hike rates in December—beating by 16.5 basis points already priced in.

Treasury pressures added further friction. Yield curve saw a sharper rise, especially at the belly, with 10‑year yields dropping roughly 10 basis points. Partly, it’s the typical month‑end rebalancing, but there’s a stronger push for investors to lock in yields as the Fed cuts the fed‑funds rate.

Equities: Riding the Skyward Trend

In the equities arena, the S&P 500 crept up ~0.6% to close the week—a 6% monthly gain, the best in a year. It also hit its 53rd all‑time 2024 close, ranking as the 5th best of any year on record. I stay bullish toward year‑end: earnings and growth hold sway, but fresh capital might dry up, leaving the final weeks dominated by portfolio trimming and window dressing.

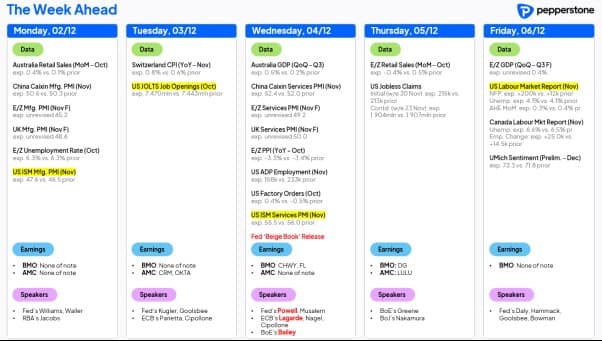

Looking Ahead: A Busy Week in the Books

What’s on the horizon: a jumble of manufacturing PMI releases that likely signal a fairly grim industrial outlook. The US ISM figures—especially the employment sub‑index—will be in the spotlight before the jobs report drops.

Stay tuned for the latest U.S. labor market numbers on Friday, which are sure to ignite a flurry of activity across financial markets.

Keep Your Finger on the Pulse!

Never miss a beat from this post category again. Subscribe now and get real‑time updates delivered straight to your device—no more scrolling, no more waiting.

- Instant alerts as soon as new content drops

- Stay ahead with premium notifications

- Easy, one‑click sign‑up

Subscribe