June’s Labor Market Teaser: A Mixed‑Bag Update

As the calendar flips to the first Friday of the month, investors and economists alike get a fresh look at the US labor market. June’s employment data is creeping up on the horizon, marking the end of the first trading week of the second half of 2024.

What’s the buzz from May?

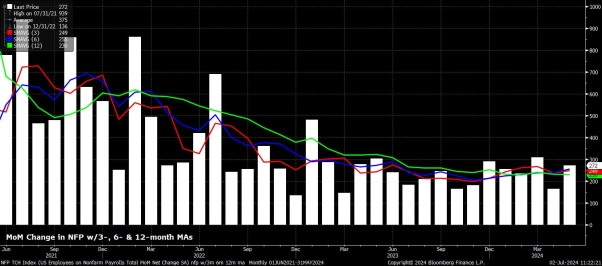

- Strong headline: Non‑farm payrolls hit an unexpected +272k in May.

- Higher unemployment: The number of people looking for work rose, throwing a wrench into the optimism.

- Expectations for more clarity now echo louder—especially with a potential Fed rate cut in the summer months still in the backseat.

June’s Forecasts: Speed‑bump vs. Smooth Ride

Market analysts project a softer jump for job creation—around a +200k increase in June—slowing down from May’s pace. This figure sits below both the 3‑month average and the breakeven threshold, each hovering near +250k.

Interestingly, the spread of predictions is razor‑thin, ranging from +140k to +237k. That’s the tightest variance we’ve seen since late 2018, a 4.4‑deviation spread compared to the usual 5.5—hinting that the next report might swing outside expectations.

In Summary

With June’s numbers expected to settle the book on employment growth, traders are keeping a close eye on these figures. The Fed’s potential rate cut hangs in the balance, so keep your eyes peeled for surprises.

Payroll Play: A Slightly Sloping Slide in the Workforce Landscape

The latest headline payroll print nudged a tad downward, but it’s not too bad. Think of it like a mild drizzle on a sunny day—just enough to dampen the vibe but still enough sunshine to keep things moving.

Unemployment Claims: Ooh, the Numbers are Lifting!

- Initial claims: Up by 23,000 from May to June.

- Continuing claims: Climbed by 49,000, hitting the highest level since November 2022.

So, while job openings are still going strong, more folks are seeking help, which could hint at a slightly chilling labor market.

Manufacturing’s Hidden Drop: The ISM Survey Says…

June’s ISM manufacturing survey looked a bit gloomy for employment, dropping the sub‑index from 51.1 to 49.3—a subtle but notable dip. It’s almost as if factories decided to hit the pause button on hiring.

What’s Next? Services & ADP—A Mixed Bag

The upcoming services gauge releases this Wednesday, so we’ll get a fresh glimpse into that sector. As for the ADP employment figure—well, let’s just say it’s become a bit of a rogue wave, diverging from the official BLS jobs data for years. If you’re looking for reliable noise, skip it.

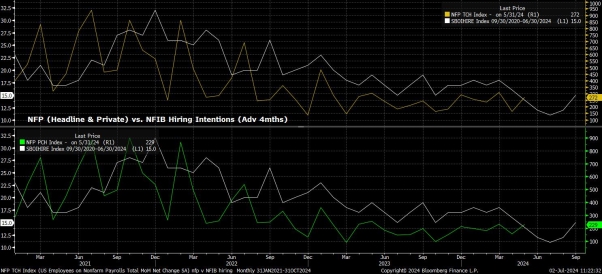

The NFIB Hiring Intentions: A Sneak Preview of Future Trends

The NFIB’s gauge captures both headline and private payroll growth for the current cycle but lags a few months. It currently forecasts a modest slowdown in job growth for June, predicting roughly 170,000 new jobs. However, the indicator hints that this flattening might just be a summer lull, and the bottom could be near for the season to end.

Takeaway

All in all, the workforce is feeling a bit wind‑turbulent—claims are rising, automation in manufacturing might be cooling, and private hiring intentions suggest a slight pause. Keep an eye on next week’s services data and try not to chase the ADP numbers too hard.

Money Talks: June’s Wage Growth Takes a Gentle Slide

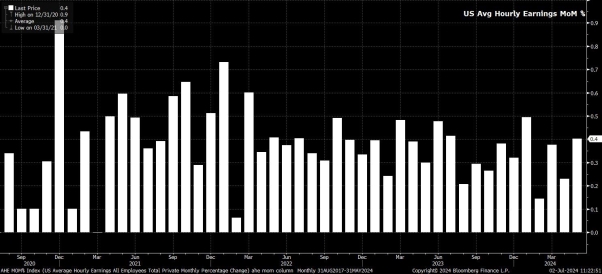

What the numbers are saying: July’s payroll data tells a story of slightly easing pay‑pressure. In May workers saw the fastest hike in hourly rates since January, but June’s strength is a smidge less forceful.

Key figures in a nutshell

- Hourly earnings: up 0.3% month‑on‑month—a 0.1 percentage‑point dip compared to May.

- Annual growth: steady 3.9% versus 4.1% last month.

So, what does that mean for the economy? Picture a pothole‑laden road slowly steering back towards that coveted 2% inflation target. The labour market? The hint of a gentle “relaxation” as hiring and wages start to tap their foot.

Why it matters

The modest slowdown suggests the economy is not doing a perfect balance‑of‑weighted‑bump‑frequent dance, but the floors are getting a little less sticky.

Takeaway

Overall, June paints a picture of a still‑tight but slowly easing labor condition—good news for minds that love a mix of steady growth and lighter inflation strides.

Labour Market: A Slow Ballet Gone Awry

Unemployment sticks at 4%, even after the last jobs report surprised everyone with a brief jump to its highest level since January 2022.

The labour force participation takes a gentle leap forward, gaining 0.1% to reach 62.6% after a notable dip the previous month.

However, the household survey feels like a can’t-make-up-mind dance—its numbers swing wildly, thanks in part to a surge in immigration that’s skewing the data. This explains why the household and establishment surveys keep pulling at different strings.

What the Numbers are Telling Us

- Establishment data remains the steady, dependable headline—think of it as the calm conductor in a turbulent orchestra.

- Household data rides a roller‑coaster, making it hard to pin down any clear trend.

- The overall picture is one of a slowly loosening labour market, not a dramatic crash.

Bottom line: if you want a reliable reading of the job market, keep your eyes on the establishment survey—it’s the one that really knows how to stay on track.

June Jobs Report: A Calm Day for Markets, but With a Twist

All in all, the June jobs data looks to be another gentle reminder that the labor market is slowly easing back into its usual rhythm. And, as it turns out, that’s right on point with what the Fed’s latest Economic Forecasts were expecting.

Policy Take‑away: Inflation Still Wins The Referendum

- Inflation king. The Fed’s top priority remains price stability—so even if employment looks a tad sturdy, the halls of the Federal Reserve are still humming to the inflation beat.

- Powell’s warning. Chair Powell has made it clear that only a sudden, unexpected slump in the job market would push the Commission to change gears. Until there’s real confidence that prices are sliding back toward the 2% target, the Fed’s thumbs stay out.

What the Markets Are Likely to Do…

With the data dropping on July 5th – a day that sits snugly after Independence Day – the market’s response is set to be fairly subdued. Think of that period like a quiet holiday: nothing loud, nothing noisy.

- Low volumes, thin liquidity. It’s a “home‑office” type of day. Most traders will be on their couches, enjoying the long weekend, leaving the trading floor relatively light.

- Expectation vs. surprise. If the numbers match forecasts, you won’t see anything dramatic. But if the data overshoots or falls short—above or below the narrow window—we might see a spike in reactions because the market’s been riding on thin conditions.

- Risk management rules. Even with the light touch, keep your risk controls tight—because a surprise can still punch out big.

Key Takeaway

In short, the June jobs announcement is another gentle nudge toward normalization. Inflation keeps the Fed’s focus, the markets stay calm (mostly), and traders are taking a breather. But stay ready: if the data wiggles out of line, the impacts could feel big.