November Labor Market: A Mixed Bag That Leaves Us With More Questions Than Answers

There are a handful of data points to chew on, but the overall picture feels like a puzzle with some missing pieces. While the markets celebrated fresh highs, the latest labor numbers leave both traders and policy-makers a little puzzled.

What the Numbers Say

- Jobs added in November: 227 k – just a touch above what most of us expected and a little shy of my own 235 k guess.

- The three‑month moving average of job growth has just hit its highest since May—thanks to revisions that nudged earlier figures up by 56 k.

- Much of that growth simply un‑winds the weather‑ and strike‑related losses that were recorded a month earlier.

- Average hourly earnings kept climbing at a steady pace: 0.4 % MoM, 4.0 % YoY, unchanged from October. Hawks in the Federal Open Market Committee (FOMC) might want to see a slowdown sooner rather than later.

- Unemployment rose to 4.2%—close to the 4.3% peak from July—while labor force participation dipped to 62.5%, its lowest level since May.

Why This Feels Like a Head Scratch

The paradox here is simple: job gains are strong, wages tick up, but unemployment is creeping upwards. It’s another one‑of those “what’s the realistic outlook” moments that market participants and policymakers might debate for days.

From a policy perspective, the rise in unemployment could help justify a 25‑basis‑point rate cut in December—especially if we want to keep a “path of least regret” in mind. If there are concerns about stalling disinflation or potential inflation bubbles in early 2025, the Fed might consider skipping the January meeting altogether.

Stock Market Response

Despite the data’s odd timing—when liquidity is thin and trading volumes are light—stocks closed higher. The tech‑heavy Nasdaq led the charge, while the S&P 500 hit its 57th all‑time close of the year. With only 16 trading days left, breaking 1995’s record of 77 ATHs is unlikely, but the bulls remain in control. Dips can still be seen as buying opportunities, though confidence may taper as the year winds down.

The Dollar’s Move

The USD was a bit choppy after the non‑farm payroll report but still managed a modest weekly gain, now on its ninth gain in ten against a range of peers. I remain convinced that further USD upside is plausible, especially if FOMC outlooks become more two‑sided toward 2025 and the U.S. economy keeps outperforming its peers. Any spikes in geopolitical risk—like weekend flare‑ups in Syria—could give the dollar a boost from a haven‑demand perspective.

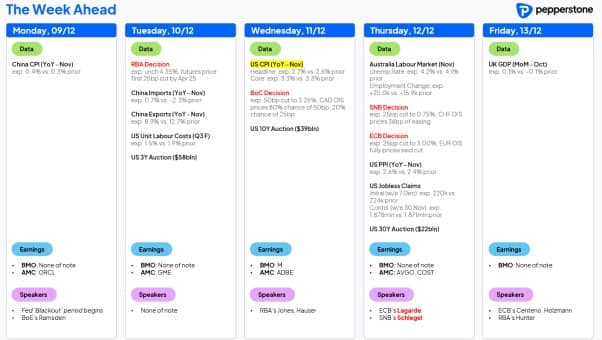

What to Expect This Week

Today sets a quiet tone, but a bustling week is on the horizon. The data docket in the next 24 hours won’t bring much sauce, but we’re in the pre‑meeting “blackout” period for the Fed.

- Central bank policy moves coming: The Bank of Canada, Swiss National Bank, and European Central Bank all aim to announce rate cuts.

- U.S. CPI data will again help shape the week’s narrative.

Overall, the market’s outlook remains buoyant, but the data this week should be watched closely—especially for any further nudges that could signal shifts in the pendulum of economic policy.

Stay Ahead of the Curve—Real‑Time Alerts Right in Your Pocket!

Ever feel like you’re missing out on the latest buzz in your favorite category? Don’t worry—you can catch every update before anyone else does. Just subscribe now and let the phone do the heavy lifting for you.

Why hit that subscribe button?

- Instant Delivery: Get the news the moment it goes live.

- Zero FOMO: Never miss a headline or a hot topic again.

- Curated Experience: Only receive content you actually care about.

- One‑Tap Control: Manage preferences in seconds—no tedious settings.